We have been purchasing notes, mortgages and real estate contracts for over a decade and we pride ourselves on a unique client experience at the best price possible.

Owner-financing, also called seller-financing, is a term used for properties or businesses that have been sold privately, without the use of a traditional bank to lend the borrower/buyer money. Instead, the seller of the collateral (a business or a property) will finance the sale themselves and carry back a mortgage note or a carry back business note. So why is it important to learn about owner financed mortgage or business notes when selling a property or business?

The property or business seller will act as the bank collecting interest on the money they lend. This transaction can be very beneficial to both buyer and seller as it allows the property sale to move much quicker than traditional transaction using a bank and real estate agent, etc. In addition to the streamlined process, the borrower does not have to prove income and debt-to-income, which usually will not be possible with a bank.

Chances of Success Using Owner-Financed Notes

A good candidate for whom to carry an owner-financed mortgage note or business note is a person that has a decent credit score and the ability to put down an above-average down payment. A business or property seller using a seller-carry back note to move a their collateral quickly must perform a small amount of diligence in order to minimize their exposure to risk down the road. Risk is a term used to describe the possibility of default/non-payment, or property value decreasing, among others. Most people thinking about creating a seller-financed note do not usually like the idea of being a bank for the next 10 to 30 years (depending on the loan’s structure), which is why we offer an exit strategy that most owner-financed note holders overlook which is: selling the seller carry-back note to note buyers once the sale has been completed.

Creating a Valuable Mortgage Note to Sell to an Investor

When Seller-Financing (or owner-carrying) a business note as the result of a small business sale is one of the very few options left for small business sellers in this downed market. If you do plan on seller-financing a small business sale over the next five to ten years, rest assured that there is a sound exit strategy for you and/or you corporation/client. This consists of creating the most valuable business note possible in order to resell it on the secondary loan market for a lump sum of cash. Learn How to Create a Valuable Mortgage Note to Sell

Creating a Valuable Business Note to Sell to an Investor

When Seller-Financing (or owner-carrying) a mortgage note as the result of a property sale is becoming the “norm” in the downward-leaning economy, and as most people see it, we are in it for the long haul. If you do plan on seller-financing a property sale and you want to simply sell the mortgage note instead of playing the bank, rest assured that there is a sound exit strategy for you. This consists of creating the most valuable mortgage note possible in order to resell it on the secondary loan market for a lump sum of cash. Learn How to Create a Valuable Business Note to Sell

A Complete Guide to Owner Financing

Whether you’re in the market to buy or you’re ready to sell your home, it’s not always possible to get a bank involved in the process. When that happens, owner financing can be a way for buyers and sellers to reach an agreement without all of the red tape.

Read on below to learn more about what owner financing is, how it works, and what you need to know before creating a seller financing agreement of your own.

What is owner financing in real estate?

Also known as “seller financing”, owner financing is a method that can be used to purchase real estate if the buyers are unable to obtain a traditional mortgage. In this type of arrangement, instead of taking out a mortgage and making regular payments on it to a bank, the buyers make their payments directly to the sellers. It’s important to note that owner financing deals are still legally-binding financial arrangements. In order to make this type of financing work, an agreement must first be reached between the buyers and the sellers. Typically, the buyers promise to pay the sellers in monthly installments, which include principal and interest, until the property has been paid off at the full purchase price. Once an agreement has been reached, it must also be put in writing. The paperwork used is fairly standard and includes a mortgage and mortgage note, or deed of trust.

How it works: an owner financing example

In this example, let’s say the buyers saw a $200,000 house that they intend to buy. However, when they went to their bank to get approved for a loan, they were denied. Maybe their credit isn’t the best or maybe they’re full-time investors who’ve reached their financing limit, but whatever the reason, they won’t be able to go through traditional channels to finance the home. In that case, the buyers could approach the sellers and ask them to consider an owner financing arrangement instead. Here, rather than receiving the proceeds from the sale of their house in a lump sum similar to how they would with bank financing, the sellers would receive the funds in monthly installments. However, in exchange for their flexibility, in addition to the purchase price, they would also receive 6% interest on the 15-year loan. In the above scenario, the financing would break down as follows:

What are the advantages of owner financing?

Like any other type of financial arrangement, there are some distinct advantages to using this type of financing over a bank loan. They’re listed below for your consideration.

Pros for the Buyer

It gives you the opportunity to become a homeowner: If you can’t qualify for traditional financing, your options for buying a home are more limited. Seller financing gives you the opportunity to become a homeowner without having to have enough money in hand to buy the property in cash.

There’s more flexibility: Since your loan will never be sold and repackaged, it’s not subject to the same guidelines as most bank loans. This means that you have more flexibility in terms of what you can negotiate for the down payment, loan term, and interest rate.

There are fewer closing costs: When there’s no mortgage company involved, you don’t have to worry about paying any of their fees – like an application fee and origination fee – which can make your purchase cheaper upfront.

You can close on the home faster: Closing on a traditional mortgage typically takes 30-60 days and the bulk of that time comes from the bank needing to verify that you qualify for a loan. When there aren’t those traditional qualifying standards in place, it’s possible to close much faster.

Pros for the Seller

There’s the potential for passive income: Sellers looking for a source of monthly income may benefit from this option because it offers the opportunity to receive regular monthly payments.

But there’s still an option to get paid in a lump sum: Alternatively, if you’d rather get paid in a lump sum, think about the possibility of selling real estate notes to an investor and receive payment right away.

There are often fewer contingencies: Often, mortgage companies require certain contingencies – like conducting a satisfactory appraisal or making specific repairs – to be met in order to provide financing for the home. With seller financing, meeting those conditions is no longer a requirement.

The closing time is shorter: As mentioned above, it’s often possible to close on a home more quickly with seller financing because the buyer does not have to go through the underwriting process.

What are the disadvantages of owner financing?

That said, using seller financing to buy or sell a home also comes with a few disadvantages. Be sure to look over them carefully so you can decide if seller financing is a good fit for you.

Cons for the Buyer

There’s no guarantee that the sellers will agree: Like the other details in a purchase offer, owner financing is a point of negotiation. Put simply, while you can ask for it, there’s no guarantee that the seller will agree.

You’ll likely have to provide incentives for the sellers: If you do decide to ask for seller financing, you’ll likely have to provide some incentives to make this arrangement worth it for the sellers. As a result, the mortgages on most owner financing homes come with higher interest rates or larger down payments than you would expect to see with a bank loan.

You’ll need to watch out for a due on sale clause: You’ll need to be especially careful if the sellers still have a mortgage on the property. Most mortgages include a due on sale clause, which entitles their lender to ask for full repayment of the loan when the property is sold. If the seller can’t pay in full because of your financial arrangement, their lender could foreclose on the property, leaving you without a home.

Cons for the Seller

There are some rules you need to follow: The Dodd-Frank Act of 2010 introduced some new regulations for owner financing. We’ll go into more about the specifics below, but it’s important to know that any agreement you make with a buyer will likely be subject to those regulations.

The buyers could default on the loan: Any time you loan someone money, which is essentially what you’re doing with seller financing, you’re taking a risk that you won’t be repaid. If the buyers decide to stop making payments, you will be the one responsible for taking them through the foreclosure process.

How the Dodd-Frank Act impacts owner financing documents

At its core, the Dodd-Frank Act was created in the wake of the Great Recession in order to promote stability in the finance industry by improving transparency and accountability. While the majority of the bill is focused on debt collection and servicing, a portion of it does apply to seller financing.

Here’s what you need to know:

What are the biggest changes to seller financing?

1. When combined with the SAFE Act, the Dodd-Frank Act requires seller financing transactions to be originated by Residential Mortgage Loan Originator, who is licensed in that state in which the property is located.

2. The act prohibits builders from selling properties with owner financing

3. It also eliminates balloon payments and negative amortizing loans

4. It requires that any adjustable-rate mortgages include a fixed-rate period for at least five years with no prepayment penalties

5. Lenders must consider the borrower’s ability to repay the loan

6. Lenders must consider at least eight underwriting guidelines before approving the buyer for a loan, including the buyers’ employment status, credit history, debt-to-income ratio, and monthly payment, among others.

7. Lenders must wait at least 120 days of delinquency before foreclosing

8. Forced arbitration clauses are no longer allowed in mortgage notes

What are the exceptions under the Dodd-Frank Act?

That said, there are to the seller financing provisions under the act. They generally fall under one of three categories, each with its own set of exceptions:

Individuals and trusts that finance one property per year

The note can contain a balloon payment

The sellers do not have to prove the buyers’ ability to pay

The interest rate has to be based on the index and remain fixed for the first five years.

After that, the interest rate can only raise a maximum of six points at a rate of two points per year

Individuals and trusts that finance one to three properties per year

No balloon payment is allowed

The sellers must prove the buyers’ ability to pay

The interest rate has to be based on the index and remain fixed for the first five years.

Following, the interest rate can only raise a maximum of six points at a rate of two points per year

Any individual or entity that finances more than three properties per year

The rules are the same as for the one-to-three property group, but a Mortgage Loan Originator must be involved in the transaction.

Which loans are not covered by the Dodd-Frank Act?

The Dodd-Frank Act is only meant to protect residential mortgage loans, which means it does not apply to loans on the following:

Vacant land

Commercial properties

Rental or investment properties

Residential properties in which the buyer does not reside

Any properties purchased by non-consumer buyers, such as limited liability companies (LLCs), limited partnerships (LPs), or corporations

Important owner financing terms to consider during negotiations

With seller financing transactions, it’s up to the buyers and the sellers to come up with the terms of the financial agreement between both parties, Often, these terms can be negotiated, but here is an overview of what details you’ll need to consider:

THE LOAN TERM

The loan term refers to the length of time that it will take the buyers to repay the loan. Usually, this length of time falls anywhere between five and thirty years, but it can be any length of time that you see fit.

Typically, buyers like longer loan terms because that keeps their monthly payments lower. Sellers, on the other hand, don’t want to wait a long time for their investments to pay off, so they tend to prefer shorter loan terms, with or without a balloon payment.

THE BALLOON PAYMENT

A balloon payment isn’t a requirement for owner financing homes, but they are commonly used. With balloon payments, the buyer makes fixed monthly payments for a short period of time, usually a few years, before making a large, lump-sum payment to pay off the remainder of the loan.

It’s up to the buyers to determine how they want to finance that lump-sum payment, but it usually happens via pulling from savings, refinancing the loan, or selling the property.

THE DOWN PAYMENT

A down payment is an amount of money that the buyers use to indicate their interest in buying the property. They give this money to the sellers upfront as a “good faith deposit” toward buying the home. The remainder of the purchase price after the down payment is what gets financed.

Typically, down payments range anywhere between 3%-20% of the home’s purchase price. However, with owner financing, it is not uncommon to see larger down payments used as an incentive for the sellers to accept the alternative financing arrangement.

THE INTEREST RATE

The interest rates on rates on seller-financed properties are also typically higher than you might see with a bank loan. In most cases, it’s because the sellers are taking on some risk in financing the property and the higher interest rate is meant as compensation. With that in mind, it’s not uncommon to see interest rates ranging from 4%-10%.

However, in addition to the interest rate itself, you also have to decide how the interest will accrue. Here is an overview of your options:

FIXED-LOAN RATE

With a fixed-rate loan, both the interest rate and the principal loan amount stay the same over the life of the loan. Many buyers and sellers prefer this type of loan because it is easier to keep track of for accounting purposes and it means that the buyers are able to predict their monthly payments.

ADJUSTABLE LOAN RATE

With this type of loan a low, introductory interest rate is offered for a few years. However, after that introductory-rate period is up, the interest rate adjusts periodically.

INTEREST-ONLY LOAN

When using an interest-only loan, the buyer only makes payments on the interest that accrues from the loan for a set period of time. Then, a balloon payment is made in order to pay off the principal loan amount.

How to structure an owner financing contract

The last thing you need to be aware of is the proper way to structure an owner financing contract. There are a few different methods that you can choose from, but keep in mind that the structure that you pick will affect the buyers’ ownership stake in the property and the process for foreclosure in the event that they default.

Mortgage (or deed of trust) and mortgage note

This is the most common structure, as it is the same process that a bank uses when they issue a loan. In this case, there are two important documents that need to be created:

The mortgage note: A mortgage note outlines the repayment terms for the loan. It should be kept by the seller.

The mortgage or deed of trust: Depending on where you live, you’ll also need to draw up either a mortgage or a deed of trust, which will hold the home up as collateral in the event that the buyers default on their promise to repay the loan.

This is typically considered the most secure form of ownership for the buyers and the sellers because the buyers will be put on the title and given a deed while the mortgage will be recorded and stored in public records.

Contract for deed

Also known as an “Agreement for deed”, this contract is structured in the same way as a mortgage and promissory note. However, instead of the buyers being placed on the title right away, the sellers remain on the title until the loan is paid off in full.

Sellers often prefer this structure because it’s often cheaper and easier than the alternative. Plus, since they remain on the title, the foreclosure process is often easier if the buyers default. However, not all states recognize this type of contract.

The Bottom Line

Seller financing is an alternative to the traditional bank loan. While this type of financing can have distinct benefits for both parties, it does still involve signing a legally-binding agreement. In light of that, it’s important to consult with an attorney or financial professional if you have any questions during this process. However, at the end of the day, owner financing can be an effective way to create a financing arrangement that truly suits your needs.

Written By

Tara Mastroeni

Tara Mastroeni is a real estate and personal finance writer. Her work has been published on websites such as Forbes Advisor, Business Insider, and The Motley Fool. See full bio.

Edited By

Molly Corson

Molly Corson is the Co-Founder and Marketing Director at Amerinote Xchange. Molly's diversified background and experience lies in the areas marketing ad-tech, team-building, operations-management, sales and strategic relations management. Molly has a BA degree from Temple University. See full bio.

Financially Reviewed By

Abby Shemesh

Abby is the co-founder and Chief Acquisitions Officer at Amerinote Xchange. He has been operating within the mortgage market for over a decade.

Abby was featured on industry publications like Yahoo! Finance, MSN Money, Realtor.com, and GOBankingRates.com. See full bio.

A good candidate for whom to carry an owner-financed mortgage note or business note is a person that has a decent credit score and the ability to put down an above-average down payment. A business or property seller using a seller-carry back note to move a their collateral quickly must perform a small amount of diligence in order to minimize their exposure to risk down the road. Risk is a term used to describe the possibility of default/non-payment, or property value decreasing, among others. Most people thinking about creating a seller-financed note do not usually like the idea of being a bank for the next 10 to 30 years (depending on the loan’s structure), which is why we offer an exit strategy that most owner-financed note holders overlook which is: selling the seller carry-back note to

A good candidate for whom to carry an owner-financed mortgage note or business note is a person that has a decent credit score and the ability to put down an above-average down payment. A business or property seller using a seller-carry back note to move a their collateral quickly must perform a small amount of diligence in order to minimize their exposure to risk down the road. Risk is a term used to describe the possibility of default/non-payment, or property value decreasing, among others. Most people thinking about creating a seller-financed note do not usually like the idea of being a bank for the next 10 to 30 years (depending on the loan’s structure), which is why we offer an exit strategy that most owner-financed note holders overlook which is: selling the seller carry-back note to  When Seller-Financing (or owner-carrying) a business note as the result of a small business sale is one of the very few options left for small business sellers in this downed market. If you do plan on seller-financing a small business sale over the next five to ten years, rest assured that there is a sound exit strategy for you and/or you corporation/client. This consists of creating the most valuable business note possible in order to resell it on the secondary loan market for a lump sum of cash.

When Seller-Financing (or owner-carrying) a business note as the result of a small business sale is one of the very few options left for small business sellers in this downed market. If you do plan on seller-financing a small business sale over the next five to ten years, rest assured that there is a sound exit strategy for you and/or you corporation/client. This consists of creating the most valuable business note possible in order to resell it on the secondary loan market for a lump sum of cash.

When Seller-Financing (or owner-carrying) a mortgage note as the result of a property sale is becoming the “norm” in the downward-leaning economy, and as most people see it, we are in it for the long haul. If you do plan on seller-financing a property sale and you want to simply sell the mortgage note instead of playing the bank, rest assured that there is a sound exit strategy for you. This consists of creating the most valuable mortgage note possible in order to resell it on the secondary loan market for a lump sum of cash.

When Seller-Financing (or owner-carrying) a mortgage note as the result of a property sale is becoming the “norm” in the downward-leaning economy, and as most people see it, we are in it for the long haul. If you do plan on seller-financing a property sale and you want to simply sell the mortgage note instead of playing the bank, rest assured that there is a sound exit strategy for you. This consists of creating the most valuable mortgage note possible in order to resell it on the secondary loan market for a lump sum of cash.

Whether you’re in the market to buy or you’re ready to sell your home, it’s not always possible to get a bank involved in the process. When that happens, owner financing can be a way for buyers and sellers to reach an agreement without all of the red tape.

Whether you’re in the market to buy or you’re ready to sell your home, it’s not always possible to get a bank involved in the process. When that happens, owner financing can be a way for buyers and sellers to reach an agreement without all of the red tape.

Also known as “seller financing”, owner financing is a method that can be used to purchase real estate if the buyers are unable to obtain a traditional mortgage. In this type of arrangement, instead of taking out a mortgage and making regular payments on it to a bank, the buyers make their payments directly to the sellers. It’s important to note that owner financing deals are still legally-binding financial arrangements. In order to make this type of financing work, an agreement must first be reached between the buyers and the sellers. Typically, the buyers promise to pay the sellers in monthly installments, which include principal and interest, until the property has been paid off at the full purchase price. Once an agreement has been reached, it must also be put in writing. The paperwork used is fairly standard and includes a mortgage and mortgage note, or deed of trust.

Also known as “seller financing”, owner financing is a method that can be used to purchase real estate if the buyers are unable to obtain a traditional mortgage. In this type of arrangement, instead of taking out a mortgage and making regular payments on it to a bank, the buyers make their payments directly to the sellers. It’s important to note that owner financing deals are still legally-binding financial arrangements. In order to make this type of financing work, an agreement must first be reached between the buyers and the sellers. Typically, the buyers promise to pay the sellers in monthly installments, which include principal and interest, until the property has been paid off at the full purchase price. Once an agreement has been reached, it must also be put in writing. The paperwork used is fairly standard and includes a mortgage and mortgage note, or deed of trust.

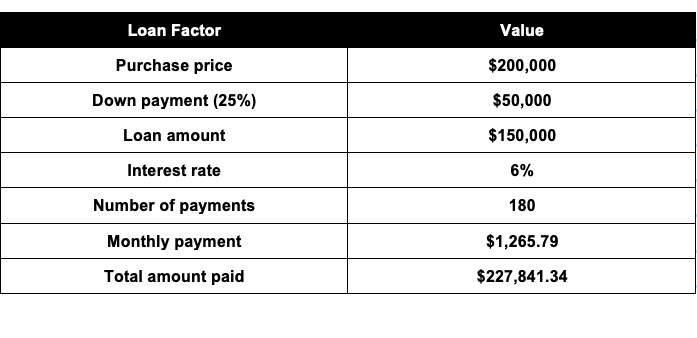

In this example, let’s say the buyers saw a $200,000 house that they intend to buy. However, when they went to their bank to get approved for a loan, they were denied. Maybe their credit isn’t the best or maybe they’re full-time investors who’ve reached their financing limit, but whatever the reason, they won’t be able to go through traditional channels to finance the home. In that case, the buyers could approach the sellers and ask them to consider an owner financing arrangement instead. Here, rather than receiving the proceeds from the sale of their house in a lump sum similar to how they would with bank financing, the sellers would receive the funds in monthly installments. However, in exchange for their flexibility, in addition to the purchase price, they would also receive 6% interest on the 15-year loan. In the above scenario, the financing would break down as follows:

In this example, let’s say the buyers saw a $200,000 house that they intend to buy. However, when they went to their bank to get approved for a loan, they were denied. Maybe their credit isn’t the best or maybe they’re full-time investors who’ve reached their financing limit, but whatever the reason, they won’t be able to go through traditional channels to finance the home. In that case, the buyers could approach the sellers and ask them to consider an owner financing arrangement instead. Here, rather than receiving the proceeds from the sale of their house in a lump sum similar to how they would with bank financing, the sellers would receive the funds in monthly installments. However, in exchange for their flexibility, in addition to the purchase price, they would also receive 6% interest on the 15-year loan. In the above scenario, the financing would break down as follows:

At its core, the

At its core, the

That said, there are to the seller financing provisions under the act. They generally fall under one of three categories, each with its own set of exceptions:

That said, there are to the seller financing provisions under the act. They generally fall under one of three categories, each with its own set of exceptions: With seller financing transactions, it’s up to the buyers and the sellers to come up with the terms of the financial agreement between both parties, Often, these terms can be negotiated, but here is an overview of what details you’ll need to consider:

With seller financing transactions, it’s up to the buyers and the sellers to come up with the terms of the financial agreement between both parties, Often, these terms can be negotiated, but here is an overview of what details you’ll need to consider: The last thing you need to be aware of is the proper way to structure an owner financing contract. There are a few different methods that you can choose from, but keep in mind that the structure that you pick will affect the buyers’ ownership stake in the property and the process for foreclosure in the event that they default.

The last thing you need to be aware of is the proper way to structure an owner financing contract. There are a few different methods that you can choose from, but keep in mind that the structure that you pick will affect the buyers’ ownership stake in the property and the process for foreclosure in the event that they default.