With seller financing transactions, it’s up to the buyers and the sellers to come up with the terms of the financial agreement between both parties, Often, these terms can be negotiated, but here is an overview of what details you’ll need to consider:

With seller financing transactions, it’s up to the buyers and the sellers to come up with the terms of the financial agreement between both parties, Often, these terms can be negotiated, but here is an overview of what details you’ll need to consider:

THE LOAN TERM

The loan term refers to the length of time that it will take the buyers to repay the loan. Usually, this length of time falls anywhere between five and thirty years, but it can be any length of time that you see fit.

Typically, buyers like longer loan terms because that keeps their monthly payments lower. Sellers, on the other hand, don’t want to wait a long time for their investments to pay off, so they tend to prefer shorter loan terms, with or without a balloon payment.

THE BALLOON PAYMENT

A balloon payment isn’t a requirement for owner financing homes, but they are commonly used. With balloon payments, the buyer makes fixed monthly payments for a short period of time, usually a few years, before making a large, lump-sum payment to pay off the remainder of the loan.

It’s up to the buyers to determine how they want to finance that lump-sum payment, but it usually happens via pulling from savings, refinancing the loan, or selling the property.

THE DOWN PAYMENT

A down payment is an amount of money that the buyers use to indicate their interest in buying the property. They give this money to the sellers upfront as a “good faith deposit” toward buying the home. The remainder of the purchase price after the down payment is what gets financed.

Typically, down payments range anywhere between 3%-20% of the home’s purchase price. However, with owner financing, it is not uncommon to see larger down payments used as an incentive for the sellers to accept the alternative financing arrangement.

THE INTEREST RATE

The interest rates on rates on seller-financed properties are also typically higher than you might see with a bank loan. In most cases, it’s because the sellers are taking on some risk in financing the property and the higher interest rate is meant as compensation. With that in mind, it’s not uncommon to see interest rates ranging from 4%-10%.

However, in addition to the interest rate itself, you also have to decide how the interest will accrue. Here is an overview of your options:

FIXED-LOAN RATE

With a fixed-rate loan, both the interest rate and the principal loan amount stay the same over the life of the loan. Many buyers and sellers prefer this type of loan because it is easier to keep track of for accounting purposes and it means that the buyers are able to predict their monthly payments.

ADJUSTABLE LOAN RATE

With this type of loan a low, introductory interest rate is offered for a few years. However, after that introductory-rate period is up, the interest rate adjusts periodically.

INTEREST-ONLY LOAN

When using an interest-only loan, the buyer only makes payments on the interest that accrues from the loan for a set period of time. Then, a balloon payment is made in order to pay off the principal loan amount.

A good candidate for whom to carry an owner-financed mortgage note or business note is a person that has a decent credit score and the ability to put down an above-average down payment. A business or property seller using a seller-carry back note to move a their collateral quickly must perform a small amount of diligence in order to minimize their exposure to risk down the road. Risk is a term used to describe the possibility of default/non-payment, or property value decreasing, among others. Most people thinking about creating a seller-financed note do not usually like the idea of being a bank for the next 10 to 30 years (depending on the loan’s structure), which is why we offer an exit strategy that most owner-financed note holders overlook which is: selling the seller carry-back note to

A good candidate for whom to carry an owner-financed mortgage note or business note is a person that has a decent credit score and the ability to put down an above-average down payment. A business or property seller using a seller-carry back note to move a their collateral quickly must perform a small amount of diligence in order to minimize their exposure to risk down the road. Risk is a term used to describe the possibility of default/non-payment, or property value decreasing, among others. Most people thinking about creating a seller-financed note do not usually like the idea of being a bank for the next 10 to 30 years (depending on the loan’s structure), which is why we offer an exit strategy that most owner-financed note holders overlook which is: selling the seller carry-back note to  When Seller-Financing (or owner-carrying) a business note as the result of a small business sale is one of the very few options left for small business sellers in this downed market. If you do plan on seller-financing a small business sale over the next five to ten years, rest assured that there is a sound exit strategy for you and/or you corporation/client. This consists of creating the most valuable business note possible in order to resell it on the secondary loan market for a lump sum of cash.

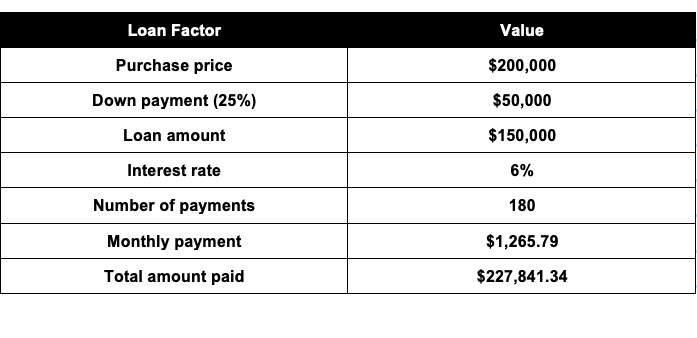

When Seller-Financing (or owner-carrying) a business note as the result of a small business sale is one of the very few options left for small business sellers in this downed market. If you do plan on seller-financing a small business sale over the next five to ten years, rest assured that there is a sound exit strategy for you and/or you corporation/client. This consists of creating the most valuable business note possible in order to resell it on the secondary loan market for a lump sum of cash.  In this example, let’s say the buyers saw a $200,000 house that they intend to buy. However, when they went to their bank to get approved for a loan, they were denied. Maybe their credit isn’t the best or maybe they’re full-time investors who’ve reached their financing limit, but whatever the reason, they won’t be able to go through traditional channels to finance the home. In that case, the buyers could approach the sellers and ask them to consider an owner financing arrangement instead. Here, rather than receiving the proceeds from the sale of their house in a lump sum similar to how they would with bank financing, the sellers would receive the funds in monthly installments. However, in exchange for their flexibility, in addition to the purchase price, they would also receive 6% interest on the 15-year loan. In the above scenario, the financing would break down as follows:

In this example, let’s say the buyers saw a $200,000 house that they intend to buy. However, when they went to their bank to get approved for a loan, they were denied. Maybe their credit isn’t the best or maybe they’re full-time investors who’ve reached their financing limit, but whatever the reason, they won’t be able to go through traditional channels to finance the home. In that case, the buyers could approach the sellers and ask them to consider an owner financing arrangement instead. Here, rather than receiving the proceeds from the sale of their house in a lump sum similar to how they would with bank financing, the sellers would receive the funds in monthly installments. However, in exchange for their flexibility, in addition to the purchase price, they would also receive 6% interest on the 15-year loan. In the above scenario, the financing would break down as follows:

At its core, the

At its core, the  That said, there are to the seller financing provisions under the act. They generally fall under one of three categories, each with its own set of exceptions:

That said, there are to the seller financing provisions under the act. They generally fall under one of three categories, each with its own set of exceptions: