Owner Financing Contract Template

Tara Mastroeni

Published: March 11, 2021 | Updated: May 16, 2025

What’s Included in an Owner Financing Contract Template? A Guide for Buyers and Sellers

While it’s easy to find an owner financing contract template online, it’s not always easy to understand what all the legal terms mean. With that in mind, below is a guide to the most important information that needs to be present in an owner finance contract. Read it over so that you understand whether the owner carry contract template that you found is a good fit for your transaction and what to do if something is missing.

Key takeaways

- Owner finance contracts are different from purchase agreements. Finance agreements list the terms of the purchase of the house.

- An owner financing agreement includes purchase price, down payment, loan balance, interest rate, payment schedule, and starting and end dates.

- Make sure to include closing costs, late fee treatments, taxes and insurance responsibilities, and treatment in case of default.

What is owner financing?

Owner financing, also known as seller financing, is a real estate transaction method in which the seller of a property provides financing to the buyer directly, bypassing traditional mortgage lenders or banks. In this arrangement, the seller acts as the lender, allowing the buyer to make payments over time for the purchase of the property, according to agreed-upon terms.

How does owner financing work?

Here’s how owner financing works: The seller offers a loan to the buyer instead of requiring bank involvement. The buyer signs a promissory note detailing the repayment schedule, interest rate, and other essential terms. The seller finances the purchase directly, and the buyer makes payments to the seller, usually every month.

This alternative to traditional financing is appealing to buyers due to credit issues or limited loan options. Since it provides an option to buy for people who might not otherwise qualify, it opens the market to more buyers. However, it also poses risk, which is why contracts often include the right to foreclose if the buyer defaults.

Until the loan is paid in full, the seller may retain a lien on the property or hold title until the buyer completes all payments. This setup can involve delayed full payment if a balloon payment is part of the structure.

Essentially, seller financing gives the seller flexibility and income potential, while offering buyers a pathway to buy a home when conventional financing isn’t feasible. That said, both parties should fully understand their rights and responsibilities and seek legal advice before finalizing any agreement.

What Are typical owner financing terms?

Though seller financing is more flexible than bank loans, most agreements follow a basic structure that reflects common contract terms in residential real estate:

- Down payment: Usually 10 to 20% of the purchase price, though it can vary based on buyer qualifications.

- Loan term: Often shorter than traditional mortgages, typically five to 10 years.

- Interest rate: May be higher than conventional rates, especially if the buyer has credit issues or cannot qualify for traditional loans.

- Monthly payments: The buyer makes regular payments of principal and interest according to the terms agreed upon.

- Balloon payment: Many owner-financing deals include a large balloon payment due at the end of the term.

- Title transfer: In most arrangements, the title to the buyer is transferred only after the buyer completes all payments. In others, the seller still has a mortgage and may structure the deal as a wraparound.

The contract should clearly outline the terms, including whether the buyer will make payments directly to the seller and what happens if there’s a buyer default. A well-drafted agreement ensures protection for both parties and prevents disputes later.

IRS rules on owner financing

When a seller extends credit to the buyer through owner financing, they must comply with IRS reporting rules just as a traditional lender would. That means reporting interest on the financing received throughout the year as taxable income. Typically, the seller must file Form 1098 if they receive over $600 in interest from the borrower in a calendar year.

The buyer, meanwhile, may be able to deduct this interest if the property qualifies as their primary residence. Since owner financing involves installment payments and often includes a balloon payment, the IRS may classify the agreement as an installment sale. This has implications for how capital gains and depreciation are reported.

It’s wise for sellers and buyers to consult tax professionals to understand the full tax consequences of structuring a contract for deed or other seller-financed arrangements. An understanding of these rules helps protect both parties and ensure that obligations are met under federal tax law.

How to ask for seller financing

Asking for seller financing requires a strategic approach, combining clear communication with a compelling proposal. Start by conducting thorough research on the property and the seller to understand their potential openness to such an arrangement. Before initiating the conversation, prepare a solid proposal that outlines the benefits of seller financing for both parties, emphasizing how it can lead to a faster transaction, potentially save on closing costs, and provide the seller with a steady income stream from the interest payments.

When you’re ready to approach the seller, do so respectfully and professionally, expressing your interest in the property and suggesting seller financing as a viable option. Be prepared to discuss your financial situation honestly, including your creditworthiness, down payment availability, and how you plan to ensure timely payments. Highlighting your commitment to maintaining the property and meeting your financial obligations can help build trust. Engaging a real estate attorney or financial advisor to assist in drafting the proposal and negotiating terms can also demonstrate your seriousness and professionalism, increasing the likelihood of a positive response.

Is an owner-financing contract the same as a purchase agreement?

First and foremost, it’s important to note that any owner financing contract template that you find needs to be used in addition to a sale agreement. These two documents serve different purposes. For its part, the purchase agreement is what allows you to transfer the ownership of the property from one person to another. The owner finance contract template lays out the terms for how the home’s purchase will be financed.

In light of that, most free owner financing contract forms are more commonly referred to as a financing addendum. This addendum is usually added to whichever real estate purchase contract most commonly used in the state where the property is located. You’ll also need a promissory note and mortgage or deed of trust to make the arrangement official.

What elements should be included in a seller finance contract template?

No one free owner finance contract template is going to be exactly the same as any other, but every contract form should include the same basic elements. To that end, we’ve laid them out below for your consideration. Read them over so that you understand what should be included in your financing addendum.

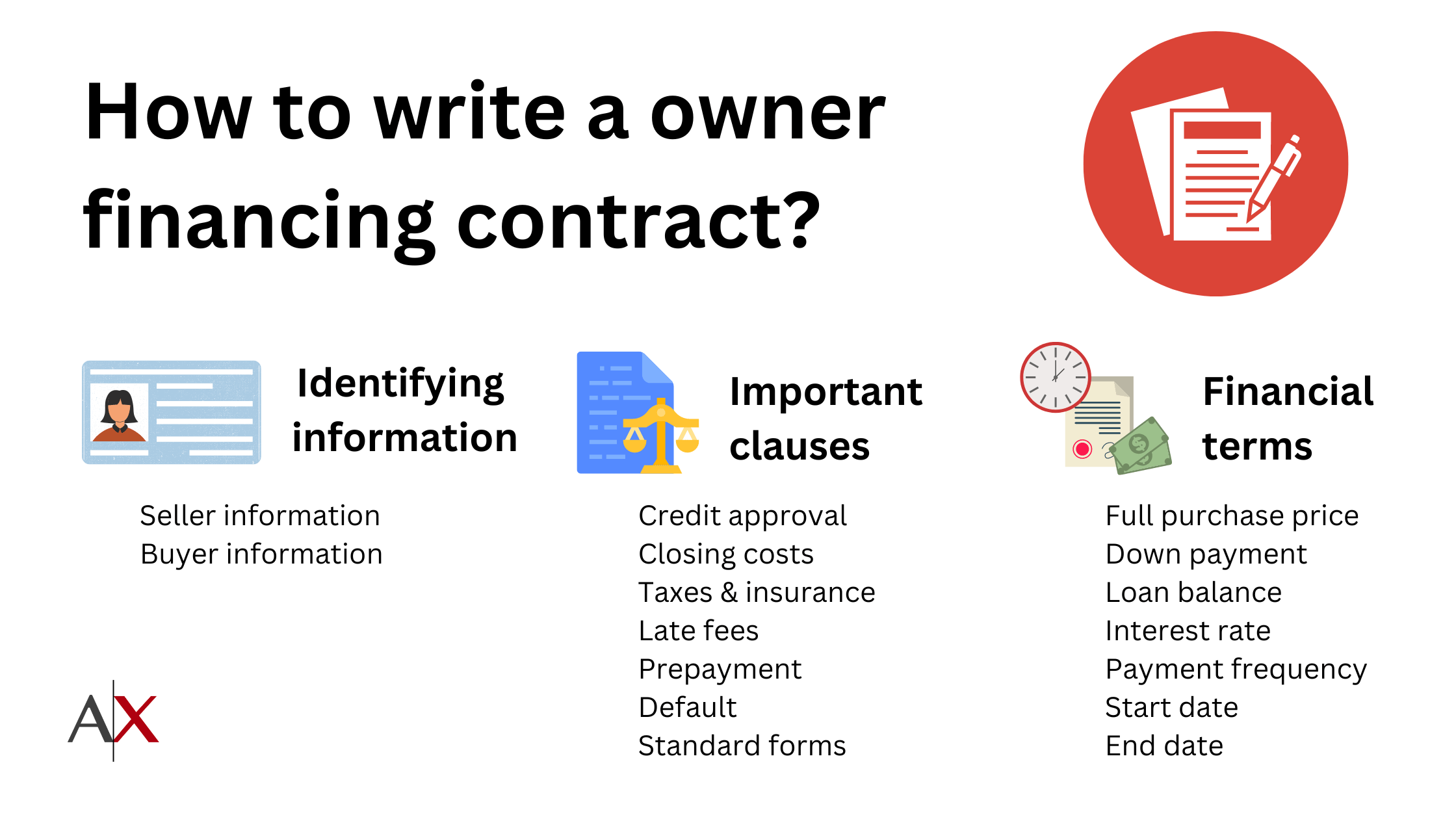

Identifying information for the parties involved

This section of the financing addendum will look like any other real estate contract. It will identify who the buyer and the seller are, the fact that the seller agrees to provide financing for the buyer, the address of the property that is being financed, and the effective date of your agreement.

Financing terms

Next, you’ll get into the financing terms. This portion of the owner finance contract template is where you will discuss the nitty-gritty details of your seller financing arrangement. It should include the following:

- Full purchase price: How much the property will be sold for in this transaction.

- Down payment amount: Sometimes the buyer will pay a portion of the purchase price upfront.

- Loan balance: The portion of the purchase price being financed, which is typically, the full purchase price minus the down payment.

- Interest rate: The amount of interest that’s being charged on the loan.

- Payment amount and frequency: How much the buyer needs to pay to the owner of a property in each installment and how often those installments occur.

- Start and end dates: The date that the buyer’s first payment is due and the date that the loan will be paid off.

Important clauses

No owner financing contract in real estate would be complete without certain clauses, which specify what will happen in the event of a particular event happening. At minimum, you need to include clauses to address the following situations:

- Credit approval: Often, an owner financing mortgage is conditional on the seller’s approval of the buyer’s credit standing.

- Closing costs: Spell out who will be responsible for covering any other costs associated with the loan, such as document preparation fees or recording fees.

- Taxes and insurance: Spell out who is responsible for paying the price for a property insurance policy and any property taxes.

- Late fees: Decide what, if any, late fees will be charged if the buyer pays late.

- Prepayment: Decide if you’ll allow the buyer to pay off their loan early or if you’ll charge them a fee.

- Default: Spell out what will happen if the buyer stops making payments on the loan.

- Standard forms: Make it clear that you will be using a promissory note and mortgage/deed of trust instruments to spell out these terms.

The bottom line on an owner financed business contract template

While you may be able to find an owner financing contract sample on the internet, you may need to do a little legwork to make them work for you. When in doubt, don’t be afraid to consult an attorney. It’s always a good idea to have a professional look over any legally-binding documents before either party signs them. A free owner-finance contract form is no exception.

Frequently Asked Questions

Can I find an owner-finance contract template online?

Yes, several websites offer free templates for real estate contracts, including those for seller financing agreements. However, it’s important to remember that not all of these templates will be created equal. Some may be more comprehensive than others, and some may not apply to your specific situation. As such, it’s always a good idea to have a professional look at any contract template before using it.

Is an owner-finance contract the same thing as a land contract?

Yes, an owner-finance contract is essentially the same as a land contract. Both are legally-binding agreements between a buyer and seller that spell out the terms of the sale, including the purchase price, down payment, interest rate, and repayment schedule.

What do I need to include in an owner-finance contract?

At a minimum, your contract should include the following:

- The names of the buyer and seller

- A description of the property being sold

- The purchase price

- The down payment amount

- The interest rate

- The repayment schedule

- The start and end dates of the loan

- Closing costs

- Taxes and insurance

- Late fees

- Prepayment

- Default

- Standard forms

You may also want to include clauses for credit approval, taxes and insurance, late fees, prepayment, and default.

Who pays property taxes on owner financing?

In an owner financing arrangement, the responsibility for paying property taxes typically falls to the buyer, even though the seller may technically hold the title to the property until the loan is fully repaid. This is because the buyer assumes the role of the property owner in practice, enjoying the use and benefits of the property from the time of agreement.