How Real Estate Investors can leverage the 721 Exchange

Jennifer Park

Published: October 14, 2022 | Updated: May 16, 2025

Selling a property can be a long and arduous process, especially if you’re looking to get the best return on your investment.

Many real estate investors are unaware of the 721 exchange, which can help them get a lump sum for their property while deferring taxes.

By leveraging the 721 exchange, real estate investors can speed up the sale process while still getting the most value for their property. This article will examine the 721 exchange in detail, including how it works and how it can benefit real estate investors.

What Is a 721 Exchange in Real Estate?

The 721 exchange, also known as the Like-Kind Exchange, is a tax-deferral strategy that allows a real estate investor to sell a property to defer capital gains taxes on the sale.

To qualify for the 721 exchange, you must exchange the sold property for another investment property of equal or greater value. Investors can use the 721 exchange for commercial and residential properties, but it must be done through a qualified intermediary.

Because this is an IRS-sanctioned process, investors can utilize the 721 tax deferred exchange to manage cash flow and reinvest in other properties without paying immediate sales taxes.

You can also use the 721 exchange to consolidate multiple properties into one larger property, which can be helpful for investors who are looking to reduce their overall portfolio size.

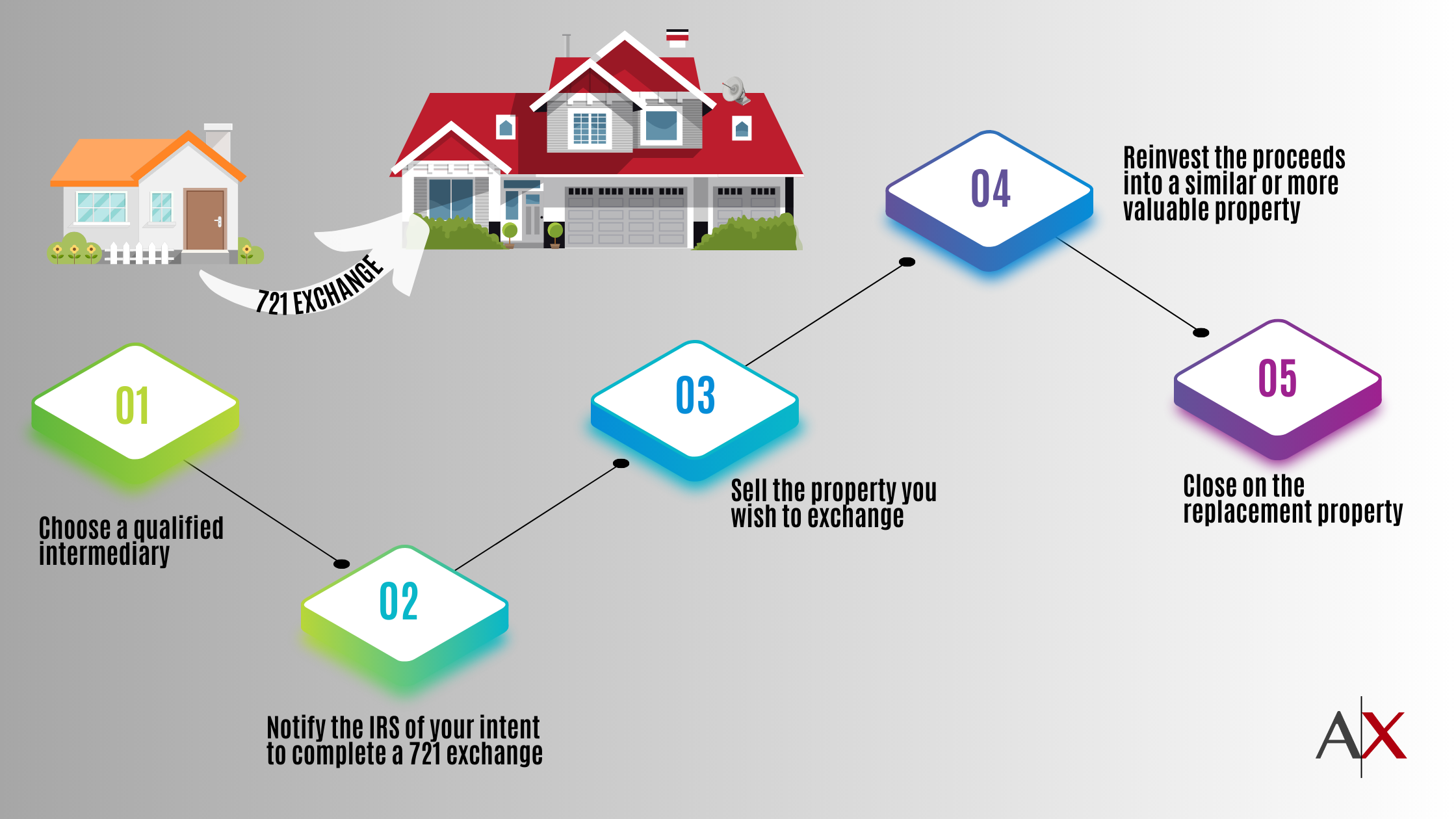

How to Complete a 721 Exchange

If you’re interested in completing a 721 exchange, there are a few steps you’ll need to follow:

- Choose a qualified intermediary.

- Notify the IRS of your intent to complete a 721 exchange.

- Sell the property you wish to exchange.

- Reinvest the proceeds into another investment property.

- Close on the replacement property.

721 Exchange Rules

To qualify for the 721 exchange, investors must follow a few key rules:

- The sold property must be exchanged for another investment property of equal or greater value.

- You must complete the exchange through a qualified intermediary.

- The sale and purchase of the properties must be completed within a specific time frame.

- Investors must notify the IRS of their intent to complete a 721 exchange.

While a section 721 exchange can be helpful for real estate investors, it’s important to note that some risks are involved. For example, investors who complete a 721 exchange and default on their loan may be subject to taxes and penalties. Additionally, if the property being exchanged is not of equal or greater value, the investor may be required to pay capital gains taxes on the difference.

Always consult a qualified tax code professional before completing a 721 exchange to ensure it is the right decision for your situation.

What Are the Primary Benefits of a 721 Exchange?

Tax Deferral

One of the most significant benefits of a 721 exchange is the ability to defer capital gains taxes. When a property owner contributes their real estate to a REIT in exchange for operating partnership units, the capital gains taxes that would typically be due upon the sale of the property are deferred. This is similar to what happens in a 1031 exchange, but the 721 exchange allows for investment into a diversified real estate portfolio rather than just one property.

Diversification

By exchanging property for shares in a REIT, an investor can diversify their investment portfolio. REITs often hold a variety of real estate assets across different sectors (such as commercial, residential, healthcare, and retail) and geographic locations. This diversification can help reduce risk, as the performance of the investment is not tied to a single property.

Liquidity

Operating partnership units received from a 721 exchange can often be converted into publicly traded REIT shares, providing liquidity that direct real estate ownership does not offer. This means that an investor can potentially convert their investment into cash more quickly and easily if needed.

Professional Management

Investors benefit from professional management of their real estate investments when they participate in a 721 exchange. The REIT manages all aspects of property ownership, operation, and maintenance, which can be a significant advantage for investors who prefer not to deal with the day-to-day responsibilities of direct property management.

Estate Planning

A 721 exchange can also be an effective tool for estate planning. By converting real estate into REIT units, property owners can more easily divide their estate among heirs. Additionally, since the units can be converted into REIT shares, they offer a more straightforward mechanism for managing inheritance compared to direct real estate, which might require heirs to manage or liquidate physical properties.

Continued Income

For many investors, the transition to a REIT through a 721 exchange means they can continue to receive income through distributions. While the specific returns will depend on the performance of the REIT and its management, this can provide a steady income stream without the hassle of managing properties directly.

1031 vs 721 Exchange

While the 1031 exchange has been getting much attention lately, the 721 exchange is a better option for most real estate investors.

The 1031 exchange allows investors to sell a property and reinvest the proceeds into another property, but it has several strict requirements.

To qualify for 1031, the exchange must include “like-kind” property. This means that the properties must be used for the same purpose and must be of similar character.

The 1031 exchange also has a much shorter timeline than the 721 exchange. Investors must identify the replacement property within 45 days of selling the original property and close on the replacement property within 180 days.

Additionally, the 1031 exchange can only be used for investment properties, whereas you can use the 721 exchange for investment and personal properties.

For most investors, the 721 exchange is a better option because it is more flexible and has a longer timeline.

Similarities Between a 1031 Exchange and 721 Exchange

Tax Deferral

The primary similarity between a 1031 Exchange and a 721 Exchange is their ability to defer taxes. A 1031 Exchange allows investors to defer capital gains taxes on the sale of a property if they reinvest the proceeds into a like-kind property. Similarly, a 721 Exchange (or UPREIT transaction) allows property owners to defer capital gains taxes by contributing their property into a real estate investment trust (REIT) in exchange for operating partnership units. In both cases, the deferral continues until the new investment is sold.

Real Estate Focus

Both exchanges are strictly used in the realm of real estate investments. The 1031 Exchange is used for exchanging like-kind properties, primarily for investment or business purposes, while the 721 Exchange involves contributing real estate into a REIT, which is inherently a real estate investment structure.

Continuation of Investment

Both exchanges allow investors to continue their investment in real estate albeit in different forms. The 1031 provides a way to move investments from one property to another, potentially upgrading or diversifying one’s real estate portfolio without the immediate tax burden. On the other hand, the 721 Exchange lets investors transition from active property management to a more passive investment form within a REIT.

Long-term Strategic Planning Tools

Investors use both 1031 and 721 exchanges as part of a long-term strategy for growing their real estate holdings and wealth over time, while managing tax liabilities. They are not typically used for short-term gains but are rather part of a larger, more strategic investment planning process.

Potential Downsides of the 721 UPREIT

The 721 UPREIT (Umbrella Partnership Real Estate Investment Trust) structure offers many benefits, such as tax deferrals and investment flexibility, but it also comes with its own set of challenges and potential negatives that interested investors should consider:

Complexity

The structure of a 721 UPREIT can be complex and difficult to understand, especially for those who are new to real estate investments. This complexity arises from the process of contributing property to an operating partnership in exchange for partnership units and later potentially converting these units into REIT shares. The legal and financial intricacies require careful navigation, often necessitating professional advice, which can add to the costs.

Lack of Liquidity

Initially, when an investor contributes property to an UPREIT, they receive operating partnership units in return, which are not as liquid as REIT shares. These units can be converted to REIT shares, typically after a holding period, but this conversion is subject to the terms set by the UPREIT, which might not always align with the investor’s liquidity needs.

Control Issues

Investors who contribute their property to an UPREIT lose direct control over their real estate. While they gain shares or units within a larger diversified portfolio, they no longer make decisions regarding the property management, leasing, or selling of the individual real estate assets they contributed.

Tax Complications

Although one of the main attractions of UPREITs is the deferral of capital gains taxes, the situation can get complicated if the REIT performs poorly or if the market conditions are unfavorable when the units are converted to shares. Furthermore, the tax implications of disposing of the shares can be significant, potentially negating some of the earlier tax advantages.

Market Risk

Like any investment, UPREITs are subject to market risks. Changes in real estate market conditions, economic downturns, or shifts in regulatory policies can impact the performance of the UPREIT. Since the investment is somewhat indirect, individual investors might feel the effects of these risks more acutely, especially if they are diversified away from their local knowledge or expertise.

Performance Dependency

Investor returns in a UPREIT are tied to the overall performance of the portfolio managed by the REIT. This means that even if an individual property within the portfolio is performing well, it could be offset by poor performance in other parts of the portfolio. This dilution of performance can affect overall returns.

Selling Mortgage Notes with 721 Exchange

If you’re a private mortgage note holder, you may wonder if you can complete a 721 exchange, the answer is yes! You can absolutely complete a 721 exchange with your mortgage note. Shares in the REIT or private mortgage note can be sold, and the proceeds can be used to purchase another property.

The tax advantages of the 721 exchange make it an excellent option for noteholders looking to sell their notes for a lump sum. You can receive a step-by-step guide to the 721 exchange process by contacting Amerinote Xchange.

Amerinote Xchange is a direct buyer of mortgage notes and can help you complete a 721 exchange with your note. Specializing in purchasing both performing and non-performing notes, Amerinote Xchange is an excellent option for noteholders looking to sell their mortgage notes quickly and for a fair price.

Whether you are estate planning or looking to free up some cash, a 721 exchange with Amerinote Xchange may be the right solution for you.

Frequently Asked Questions

Can an Investor Perform a 1031 Exchange after a 721 Exchange?

No, once an investor has performed a 721 exchange by contributing their property into a real estate investment trust (REIT) in exchange for partnership units, they cannot later use those REIT units to perform a 1031 exchange. The 1031 exchange specifically involves real estate properties, not shares or partnership units in a REIT.

After converting property into REIT units via a 721 exchange, the investor’s asset becomes a security, not a direct real estate holding. The 1031 exchange rules require that both the relinquished property and the replacement property be “like-kind,” which pertains directly to real estate. Therefore, partnership units in a REIT do not qualify as like-kind property relative to real estate, thus precluding the possibility of using them in a 1031 exchange.

Can an Investor Combine a 1031 Exchange with a 721 Exchange?

Combining a 1031 exchange with a 721 exchange is conceptually possible, but it involves a very specific sequence and timing, making it somewhat complex and less common. Here’s how it could theoretically work:

- Start with a 1031 Exchange: An investor could initially sell a property and then use the proceeds to engage in a 1031 exchange by purchasing another like-kind property. This step allows the investor to defer the capital gains tax from the original property sale.

- Transition to a 721 Exchange: After completing the 1031 exchange, if the investor eventually decides they no longer wish to manage the property directly, they could then contribute the newly acquired property into a Real Estate Investment Trust (REIT) as part of a 721 exchange. In return, they would receive units in the REIT, effectively transitioning their investment from direct real estate into a more passive form.

However, there are a few things to keep in mind:

- Timing and Ownership: The investor must meet holding period requirements to ensure that the IRS views the property as held for investment purposes rather than merely for exchange, which is critical for both the 1031 and 721 exchanges.

- Market Conditions and Opportunities: Both exchanges depend heavily on finding suitable properties and REITs willing to engage in these transactions, which can be influenced by broader market conditions.

- Tax Implications: While both exchanges aim to defer taxes, their combination needs careful planning to handle any potential tax implications correctly, especially if the transitions between them are not handled properly.

Because of the complexities and specific timing requirements, anyone considering this strategy should consult with a tax advisor or a real estate professional who has experience with both 1031 and 721 exchanges. This can help ensure that all legal requirements are met and that the financial strategy aligns with the investor’s long-term goals.

HI, I sold a 1031 replacement investment on 10/24/2022, is it too late to do 721 exchange now (2023)?

Thanks.

Jane Wu