Kentucky Foreclosure Laws and Process

Jennifer Park

Published: May 8, 2024 | Updated: May 09, 2024

Disclaimer: This is for informational purposes only. This is not legal advice. Please, consult an attorney before taking any legal action on a foreclosure or eviction.

In this article, we’ll take a closer look at Kentucky’s foreclosure laws. Since every state has its own set of rules for handling foreclosures, it’s vital for homeowners, real estate professionals, and lawyers in Kentucky to get familiar with these specifics.

Foreclosure Process Overview in Kentucky

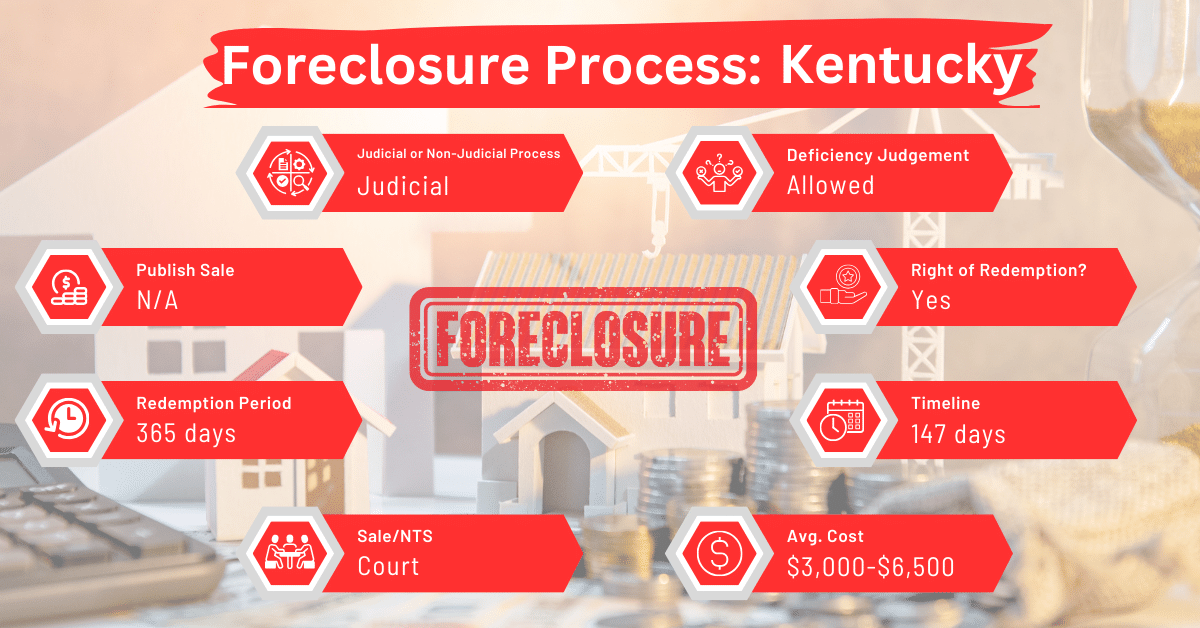

In Kentucky, foreclosures always go through the court system, with the entire process typically taking about six months—a fairly common timeframe compared to other states. Since Kentucky uses judicial foreclosures, everything starts when the lender files a lawsuit against the borrower.

Pre-foreclosure Period

The pre-foreclosure period begins with the filing of a complaint and a notice of pending action (Lis Pendens). The borrower is given 20 days to respond after receiving notice. Failure to respond leads the court to rule, potentially against the borrower, and set a foreclosure sale date. Prior to the sale, the property must be appraised.

Types of Foreclosures

In Kentucky, foreclosures must go through the courts, meaning every step requires judicial oversight.

Notice and Sale Process in a Judicial Foreclosure

Usually, a foreclosure sale happens at least a month after the court has ruled against the homeowner. Details of the sale, such as the date, location, and conditions, are published in a local newspaper for three weeks leading up to the event. A court official oversees the auction, where the highest bidder gets to buy the property. If the property sells for less than two-thirds of its appraised value, the homeowner has a year to buy it back.

Avoiding Foreclosure by Selling Your Mortgage Note

Selling the mortgage note is a practical alternative to foreclosure, providing a unique solution for borrowers. This option involves the homeowner selling their mortgage debt to a note buyer, which transfers the responsibility of the loan.

It offers a way for homeowners to avoid the long and stressful foreclosure process, giving them a faster and potentially less harmful financial outcome. This approach can be especially beneficial for those looking for immediate relief from the looming threat of foreclosure.

Borrower Rights and Protections

Kentucky law grants borrowers several rights and protections. For example, after a foreclosure sale, borrowers have a redemption period where they can reclaim their property. Additionally, foreclosures in Kentucky must go through the courts, ensuring a judge reviews the case before any action can proceed.

Redemption and Deficiency Judgments

After a foreclosure sale, borrowers have a whole year to reclaim their property, known as the redemption period. Additionally, the state permits what are called deficiency judgments. This means if the sale price of the home doesn’t cover the remaining mortgage balance, the borrower can still be held responsible for the difference.

Special Protections and Programs

In Kentucky, there are special protections and programs aimed at helping borrowers during the foreclosure process. One key feature is the state’s support for conciliation conferences. These are essentially mediation sessions where borrowers and lenders can discuss alternatives to foreclosure.

Comparative Insights

In this section, we’re going to dig into Kentucky’s approach to foreclosures and see how it stacks up against practices in other states. This comparison will help you get a clearer picture of how things are done differently across the country.

Publish Sale Notice

The law in Kentucky states that notices of foreclosure sales need to be published in a newspaper for three weeks. This is a common practice and aligns well with what you’d find in other states, such as Indiana, Illinois, and Kansas, where the length of time for publishing such notices usually falls within a similar timeframe.

Costs in a Range and Comparison to Other States

The costs of going through a foreclosure in Kentucky usually fall between $3,000 and $6,500. This is similar to many other states, where the expenses associated with foreclosure can vary quite a bit but often land within this range. It’s important to keep in mind that these costs can be influenced by a number of factors, such as legal fees, court costs, and the particular details of the foreclosure process.

Impact on Credit Score

The impact of a foreclosure on a credit score is significant, not just in Kentucky but across the United States. Experiencing a foreclosure could drop your credit score by 100 points or more. This negative effect is common in all states and sticks around on a credit report for seven years. However, its impact can lessen over time if you manage your credit well afterwards.

Conclusion

Getting a handle on Kentucky’s foreclosure laws and processes is important. Foreclosure can seem overwhelming, but there are alternatives to foreclosure, such as selling the mortgage note.