Key Information on Real Estate Owned (REO): A Comprehensive Overview

Lyle Solomon

Published: October 16, 2023 | Updated: May 16, 2025

Some terms are practically synonymous with the intricate world of real estate. Some, like mortgages, are fundamental things related to this field that everyone knows of. However, a few concepts like real estate owned (REO) are still confusing to some unless they do deep research.

The term real estate owned (REO) relates to real estate investing, working as a gateway to discounted properties and untapped market potential. Both individual home buyers and real estate investors can benefit from REO properties. But how does it work?

To understand real estate-owned properties, you need to know related things like foreclosure, how a property becomes REO property, the uses, and more. This comprehensive guide covers all that.

REO in Real Estate Meaning

Real estate owned (REO) property is a type of estate that a mortgage investor owns after the foreclosure process is over. Typically, the lender here is a government entity, a bank, or a credit union. They can use the property as collateral. This means that if the borrower defaults on the mortgage, the mortgage investor will take back the property. So, another name for REO properties is “bank-owned properties”.

The Journey from Default to REO: A Property’s Transformation

When people take a home loan, they are liable to pay the mortgage loan payments as per the pre-decided mortgage or promissory note terms. So, if they cannot pay the mortgage loan payments for over 120 days, the foreclosure process will begin.

For different people, it can be either non-judicial or judicial foreclosure. This depends on the circumstances of the case and state law guidelines that apply.

To note, the term “foreclosure” is a type of legal process in which the lender reclaims their property after the loan repayments become delinquent. The lender puts up the property for a foreclosure sale to recover the borrower’s outstanding loan balance.

During this sale, the lender can submit a credit bid on the total debt amount, including any foreclosure fees or additional costs. In exchange, they get ownership of the property. Other parties have to alternatively place a bid using cash or any equivalent of it.

REO Merits vs Demerits

You need to know what pros and cons you will face when you buy an REO property first.

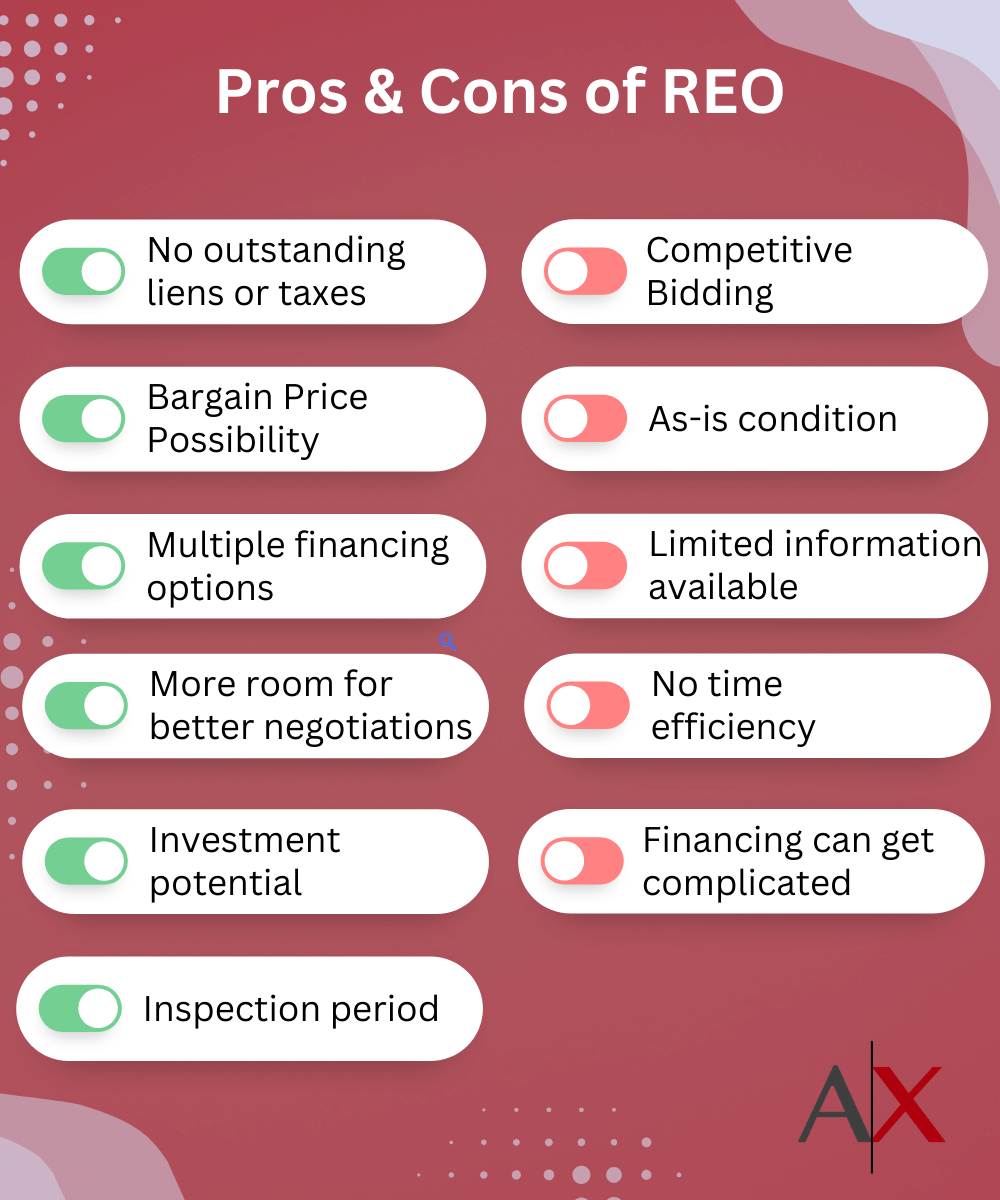

Advantages of REO:

No outstanding liens or taxes.

Home buyers must worry about outstanding liens, property taxes, and unpaid mortgage payments on the regular property they intend to purchase. Compared to that, REO properties do not come with these issues for new buyers. The lenders pay off the outstanding property taxes and liens before putting them up for sale in the REO market.

Bargain Price Possibility.

In most cases, the market value of REO properties is lower than the average property costs in the real estate market. So, if you choose to buy an REO home, you can expect quite a bargain on the house offers.

Multiple financing options.

Besides the lowered cost of REO properties, home buyers also get more financial options with this type. People who buy REO properties can apply for specialized Real-Estate Owned Loan Programs, seller financing or traditional mortgage loans. So, you can expect more secure financing support if you choose to get a foreclosed home.

More room for better negotiations.

Lenders typically provide funds to borrowers with specific terms- and that is where their responsibility ends until the borrower defaults. Holding ownership of an REO property is more of a liability since they have to pay property taxes and costs for upkeep. So, they want to sell off the REO properties as quickly as possible and are more open to negotiations. If you want more flexibility in the loan terms and purchase price, consider a REO listing more than a regular property.

Investment potential.

Real estate investors sometimes acquire properties to renovate and sell at higher costs or rent them to others for profit. The REO listings can be an excellent real estate investment for landlords and flippers since they are available at discounted prices in the REO market.

Inspection period.

REO listing agents can organize a home inspection for their clients before closing. Typically, this period lasts around ten days, and buyers can thoroughly inspect the property for issues or defects. If they see problems, they can ask for extensive repairs or negotiate a low-price deal for the bank-owned property. So, when you get a home inspection, you can ensure you receive a fair value.

Disadvantages of REO:

Competitive Bidding.

Many buyers and real estate investors show interest in REO properties due to the benefits mentioned. Naturally, with so many interested buyers, the bidding process can get competitive, and that can increase the final property cost.

As-is condition.

The bank-owned homes are often sold as is. So, the buyer who acquires the property after the bidding war will inherit the house with all of its issues, if any. Then, the buyer is liable to handle all related costs.

This is not an issue for flippers since they purchase the property to renovate it first before reselling. On the other hand, individual home buyers have to handle the maintenance or repair costs throughout their time living in the house.

Limited information available.

Lenders can hide specific information about their REO listing when they attempt to sell it. Buyers will have limited knowledge of the building’s condition or history. So, it is not a guarantee that they won’t see any issues after they move in that they did not know about before buying the real estate-owned property.

No time efficiency.

The whole legal process of purchasing the REO property is time-consuming due to the complex steps involved. The REO listing agent will help you manage the paperwork and get approvals, but it can take a long time.

Financing can get complicated.

Lenders like banks and government agencies selling REO homes may impose financing requirements on buyers. They can ask for a more significant down payment on the property and set strict terms compared to regular properties.

Steps to Buy REO houses for REO investing

The process of purchasing bank-owned properties has distinct phases.

Partner with a real estate agent.

Real estate agents are helpful with the negotiation process for REO property listings. Generally, lenders prefer dealing with professional real estate agents with a specialized understanding of lender sales and regulations. Thus, you should hire a real estate agent and submit your offer to the REO agent with their help.

Get the initial mortgage approval.

Lenders will likely trust you when they see you are serious about buying REO properties and can afford to complete the transaction. So, it would help if you got a preapproval for the mortgage offer. Submit an attested letter showing you can afford to purchase the property or make timely payments. Make sure to check what pre-qualifications you need to meet to acquire the approval status for mortgages and apply accordingly.

Find REO property listings.

You can find foreclosed properties in online portals for mortgage investors like HomePath by Fannie Mae. Besides that, mortgage lenders also manage these properties. They sell REO properties via listing agents or a foreclosure auction. You can check for multiple listing service (MLS) pages to easily search for the listed REO properties. Acquire the name and contact details of the REO agents associated with the listings you find appealing through the MLS portal.

Submit the offer.

After selecting the house you want to buy, submit the offer through the REO website of the investor or lender in charge.

Do a home inspection.

Next, you should hire a home inspector to get a home inspection on the REO property before closing the deal. In most cases, the lenders sell their REO properties without making any renovations or repairs. You can expect the property to not look the best in general. So, hire professional home inspection services to do a full survey.

Winning at REO: Pro Tips for Property Purchasers

Follow the given suggestions.

- Research the situation/process- Firstly, you should research the process of buying a real estate property, the steps that go into it, and other such details. Read about the relevance eligibility criteria to apply and do your due diligence.

- Search for properties from verified MLS platforms- Government entities like the US HUD (Department of Housing and Urban Development and mortgage lenders post their REO listings online. You should check which REO properties are available only for purchase from verified MLS sites.

- Keep some money aside for repairs first- You need to keep in mind that you must do some repairs when you buy a REO property. This is especially valid if it was a bank-owned property for a long time and remained vacant throughout.

- Clear off your available debt- Remember that the mortgage lender got the REO home because the previous mortgage holder failed to repay their mortgage loan. The lender is now selling the property and wants to be sure that the new person can pay off the outstanding balance. So, you should clear off your existing debt, if any, before submitting your offer. Take professional help with methods like debt consolidation to pay off your current debt from multiple sources in one simplified manner. Also, adopt habits like budgeting or a secondary income source to stabilize your finances.

- Prepare for tenant’s rights- If you buy a multi-tenant property with residents present, you should respect the tenant’s rights. So, learn about the related laws beforehand from sources like the Protecting Tenants at Foreclosure Act report. You must honor the active lease terms. If you have to give any eviction notice, provide residents with an introductory period of 90 days.

Who are REO properties best for?

Real estate-owned properties are better suited for real estate investors and house flippers than individual home buyers. They can quickly purchase these buildings at low price rates and use them for further profits. For example, renovating the property after purchase can add value to it. Then, they resell them at an increased rate than the purchase price or use the BRRRR method to earn passive income. The BRRRR method involves:

- Buying the property

- Renovating or Repairing

- Renting the property

- Refinancing

- Repeating the sequence with the next REO property

First-time home buyers with limited funds can also buy the REO homes since they are less costly than regular properties. However, the risk is high since they have to deal with extensive repairs, which can add to their overall expenses.

Conclusion

Overall, investing in real estate-owned (REO) properties is profitable if you do it with proper insight. Check how you qualify for this type of purchase first and assess your financial situation. There are both advantages and risks involved with buying REO properties. So, carefully consider both sides before proceeding with this type of investment compared to buying a regular property.

FAQs

What does an REO foreclosure mean?

An REO foreclosure refers to a specific stage in the foreclosure process. When a property owner defaults on their mortgage, the lender initiates foreclosure to recover the owed amount. If the property fails to sell at a foreclosure auction, often because the bid does not meet the minimum amount set by the lender, it becomes an REO property. This means that the property’s ownership transfers from the defaulted borrower to the lender, typically a bank or financial institution.

Are there commercial real estate foreclosures?

Yes, commercial real estate foreclosures do occur and operate on a similar principle as residential foreclosures. When a business or commercial property owner defaults on their mortgage, the lender may initiate foreclosure process. This process involves the lender taking legal steps to seize the commercial property, which can include office buildings, retail spaces, warehouses, or other types of commercial real estate.

Once foreclosed, these properties may be sold at auction or become Real Estate Owned (REO) by the lender if not successfully auctioned. The lender then aims to sell the property to recoup the outstanding loan balance and related costs. Commercial foreclosures can offer opportunities for investors looking to acquire properties at potentially lower prices.

Which entity typically owns a foreclosed property?

A foreclosed property is typically owned by a financial institution, such as a bank or mortgage lender. This ownership transition occurs when the homeowner defaults on their mortgage payments, leading the lender to initiate foreclosure proceedings to recoup the remaining loan balance. During foreclosure, the property’s legal title is transferred from the homeowner to the lender.

How does REO make money?

REO properties generate revenue primarily through their sale. Banks aim to sell these properties, often at market or slightly below market value, to recover the unpaid mortgage balance and associated costs. Before selling, banks may invest in maintenance or renovations to enhance the property’s appeal and value.

The selling price ideally covers the outstanding mortgage, legal fees, maintenance costs, and any renovations, with the goal of yielding a profit.

Additionally, selling these properties allows banks to eliminate ongoing expenses like property taxes, insurance, and upkeep. While banks generally prefer to minimize the time a property remains in their REO inventory due to these continuing costs, the primary revenue from REO properties comes from their eventual sale.

Which kinds of clients purchase foreclosed property?

Foreclosed properties are primarily purchased by a range of clients, each with different objectives. Real estate investors, bargain hunters, property flippers, real estate developers, and hedge funds may acquire foreclosed properties to redevelop the land or buildings for commercial or residential projects.

How does REO make money?

REO properties generate revenue when lenders prepare the property for sale and sell it after an unsuccessful sale at a foreclosure auction. Typically, the bank owned home is sold at a discount to recover the mortgage balance, foreclosure costs, and maintenance expenses.

Is REO a good investment?

Real estate owned properties can be a cost-effective investment, especially for buyers seeking homes for sale below market value of the property. However, they may require extensive repairs, so careful budgeting and inspections are crucial before buying.

Does REO mean different things in different contexts?

Yes, REO can mean different things depending on the context:

- REO meaning in mortgage: A property owned by a lender after foreclosure.

- REO address meaning: The physical location of the owned property now held by the bank or lender.

- REO sales meaning: The process of selling the REO property to recover mortgage losses.

- REO occupied meaning: Indicates the property is still occupied by tenants or the previous owner.

- REO finance meaning: Refers to mortgage or lending options used to buy REO properties.

How to get REO listings from banks?

You can find owned properties for sale by checking local real estate agents, visiting bank websites, or exploring government portals like Fannie Mae and Freddie Mac. Some banks work directly with agents who specialize in selling the REO property to speed up sales.

How to buy REO properties with no money?

To buy REOs with little or no money down, buyers can look into short sale opportunities, assume an existing home mortgage, or use hard money lenders.