How to Take Over Mortgage Payments on a Property

Tara Mastroeni

Published: February 15, 2022 | Updated: May 16, 2025

Assumable Mortgage 101: How Can Someone Take over Your Mortgage?

If you’ve ever asked the question, “Can someone else take over my mortgage?” you’re in luck. There is a way to allow someone else to take over responsibility for a mortgage. In real estate, these loans are known as “assumable loans,” and a home with an assumable mortgage may offer a buyer lower entry costs compared to a new loan

Although they are not terribly common in this market, they are a potential option for sellers who want to avoid foreclosure and buyers who may not qualify for traditional financing or who are exploring alternatives to foreclosure when buying a distressed property. If you want to learn more about how to take over mortgage payments on a property, keep reading.

We’ll go over everything you need to know about this process, including the pros and cons of taking over payments on a house, so that you have a much better idea of whether having someone take over the payments on your house is the right choice for you.

What is an assumable mortgage?

Put simply, an assumable mortgage allows a buyer to take over the seller’s existing mortgage and continue making payments under the original loan terms.

Which type of mortgage is assumable?

The most common types of assumable mortgages or loans include:

- FHA Loans: A FHA mortgage is typically assumable, allowing a qualified buyer to take over the loan without applying for a new one. This means a buyer can take over the loan without the need for a new application.

- VA Loans: Mortgages guaranteed by the U.S. Department of Veterans Affairs (VA) are also assumable. These are particularly beneficial because they offer favorable terms and do not require the buyer to be a veteran.

- USDA Loans: Mortgages guaranteed by the United States Department of Agriculture (USDA) are assumable under certain conditions.

- Some Conventional Loans: While less common, some conventional loans (those not insured by the government) may have terms that allow for assumption. This depends heavily on the mortgage lender and the specific mortgage contract.

.

In general, it is easier to take over mortgages that are backed by government agencies like the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). While a conventional loan will not typically be assumable unless the contract for an assumable clause exists, FHA loans, VA loans, and USDA loans often allow another borrower to take over responsibility for the mortgage payments on an existing loan.

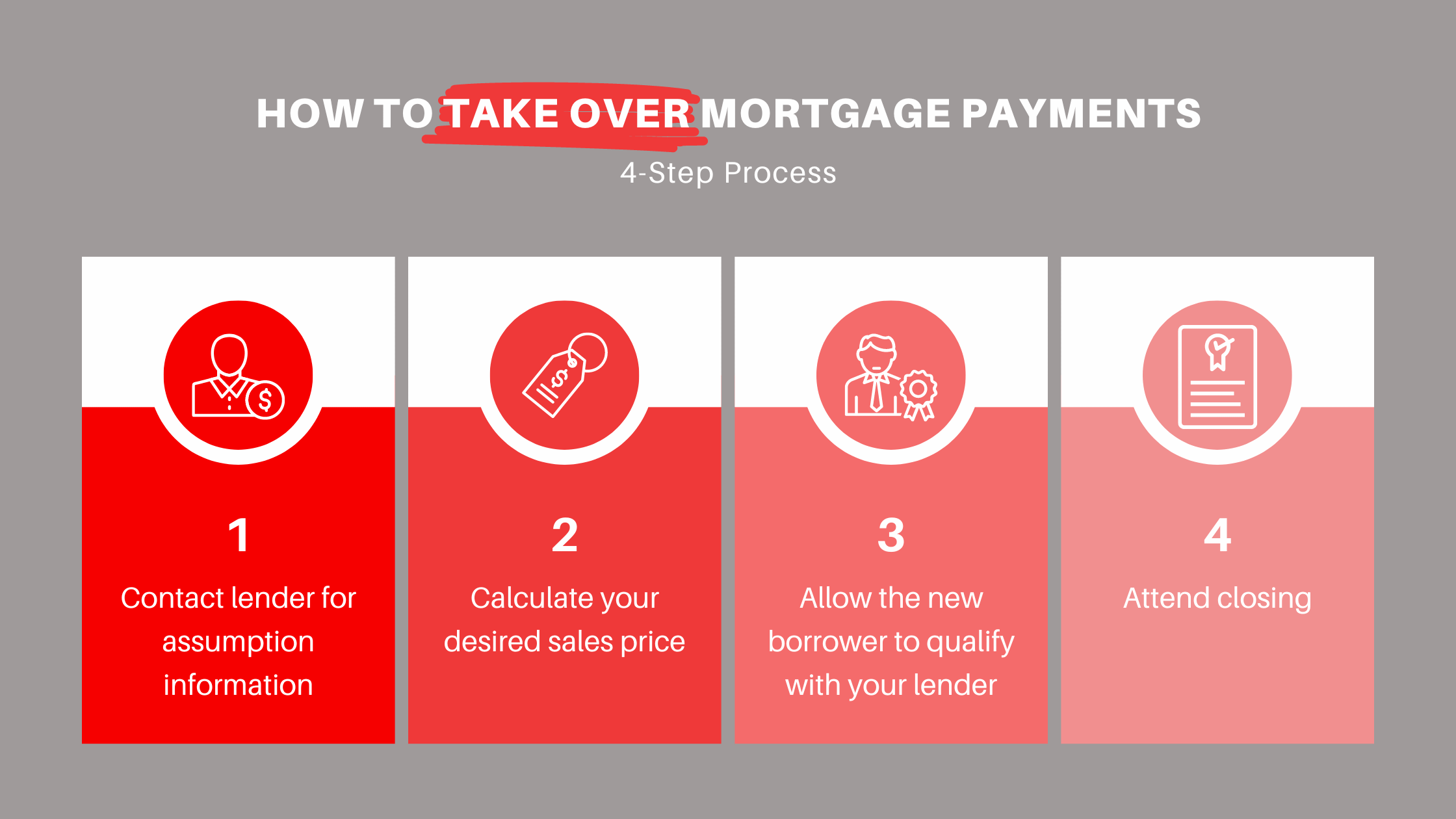

How can someone take over your mortgage?

If you think having someone else become responsible for the loan on your home may be a good idea, it’s important to have a clear idea of what the process entails before you decide to move forward.

With that in mind, here is a closer look at the steps that you need to take to complete to allow someone else to take over your mortgage payments:

- Contact your lender for assumption information: No two home loans are the same, which is why It’s important to get in contact with your lender if you would like someone else to assume your mortgage. They will be able to provide you with more specifics about the process and what you need to do to move forward.

- Calculate your desired sale price: The calculation is usually based on both the remaining balance on the mortgage and any equity in the home you’ve built up. Even if you’re open to allowing someone to assume the mortgage on your current home, you will likely want to ask for the difference between the existing loan amount and the current value of your home as a sale price. Most buyers will be able to make up this amount in a down payment or by taking out a second mortgage on the property.

- Allow the new borrower to qualify with your lender: Typically, once you find a buyer for your home, they will have to qualify with your lender to borrow the amount of the original loan and meet minimum credit score and credit and income requirements. Your lender will check their credit score and debt-to-income ratio, among other personal finance factors. Assuming everything works out, your lender will then send over an assumption package for you to fill out at closing.

- Attend closing: At settlement, paperwork will be signed and closing costs will need to be paid. On your side of the transaction, the closing costs will likely include the commission fees for the real estate agents who were involved in the deal and the cost to assume a mortgage, which may vary by loan type However, on the buyer’s side, they may include a down payment and a funding fee if they’re assuming a VA loan. Typically, the buyer will experience a significant cost savings compared to if they took out a brand new loan.

Special factors that may affect a transfer of mortgage

Transferring a mortgage isn’t always straightforward, and there are special factors that may complicate or influence the process:

- Due-on-Sale Clause: Most modern mortgages include a due-on-sale clause, which requires that the full remaining balance of the mortgage be paid when the property is sold. This can prevent assumption unless specifically waived by the lender.

- Lender Approval: Even for loans that can be assumed, the new borrower typically must qualify under the lender’s criteria. This might involve credit checks, income verification, and meeting the loan requirements tied to the original mortgage contract.

- Change in Terms: Some mortgages may allow for assumption but with adjusted terms, such as a different interest rate or different principal amount, depending on the lender’s policies.

- Liability: In some loan assumptions, the original borrower may remain liable if the new borrower defaults. Unless explicitly released by the lender. unless explicitly released by the lender, the seller may still be legally responsible for the mortgage.

The pros and cons of a buyer taking over a mortgage

Now that you know more about how assuming a mortgage works, the next step is to learn about the pros and cons of undertaking this process as the seller of the property. Read on below to learn more about if it could be the right choice for you.

Pros of a mortgage loan take over

- When interest rates are high, advertising an assumable loan may attract more buyers. One of the biggest benefits of an assumable mortgage is that it may give the seller the opportunity to advertise a mortgage with a lower interest rate than what’s currently available. For example, If the original loan has a rate of 3.5%, and rates are currently at 7%, allowing someone to assume your mortgage could help you attract more interested buyers.

- A mortgage assumption can also help with avoiding foreclosure. In this case, when someone assumes you’re deed, they become personally responsible for paying it off. If you are on the brink of foreclosure, allowing a buyer to assume the existing mortgage could be a way to halt foreclosure proceedings.

Cons of a mortgage loan take over

- Not all mortgages are assumable. Unfortunately, conventional loans often have a due on sale clause that prevents them from being assumable. If you have a conventional loan, you will likely not be able to go this route when selling your property to an interested buyer.

- Allowing someone to assume your home loan may use up your VA entitlement: Unfortunately, if you allow someone else to assume your mortgage, your VA entitlement will remain with the assumed loan. This means that you may not be able to use a VA loan program to buy a new home in the future.

Can a mortgage transfer be unofficial?

It is generally not advisable for a mortgage transfer to be unofficial. An unofficial or informal transfer of mortgage responsibility, where the new party simply starts making payments without formally assuming the loan, can lead to significant risks. These include:

- Legal Issues: If the transfer is not officially recognized by the lender, the original borrower remains legally responsible for the loan. This can lead to credit issues if payments are missed, since the original borrower is no longer responsible for the mortgage only when the transfer is done legally.

- Loan Acceleration: Most loans have clauses that can trigger a demand for immediate full repayment if the lender finds out about an unofficial transfer.

- No Legal Claim for the New Occupant: The person making payments has no legal rights to the property if they are not formally recognized by the lender and local land records.

To avoid these issues, it is vital to handle any transfer of mortgage through official channels, ensuring all legal and lender requirements are met and documented. This protects all parties involved and ensures that the property and loan rights are properly managed.

The bottom line on someone taking over the mortgage payments on your property

Many homeowners often think to themselves, “Can I get someone to take over my mortgage?” especially if they happen to be underwater on the payments. Luckily, in some cases, it is possible to have someone assume responsibility for the loan on your home.

If you’re thinking of going this route, use the information above to help you make the best decision on how to move forward. While having someone take over the mortgage payments on their property may not be the right choice for everyone, for others, it can be a viable pathway toward financial freedom.

What loan types do you see assumable mortgages working for?

And what would be a best resource for finding these sellers? Direct Mail, RE broker, Craigslist:)?…

Thank you for your time!

Thank you for your question. There are many types of loans that may be assumable. As far as strategy, we would pay attention to the property types that are suffering in this environment. That may be commercial, due to lockdowns and/or residential due to the same reasons. You would want to pay attention to Notices of Default filings in public records to see who is about to get foreclosed on. I would then cross-reference that property address to see what the sale price was and what the starting loan balance was/is. That will tell you how much equity is in the property. Most borrowers in default will not just leave the equity on the table but those borrowers who are behind on payments and have little to no equity in the property may be the perfect candidate for this type of marketing. That is, assuming your goal is to control the property through the mortgage and then make you money of rental or airBNB. I am making a lot of assumptions here but the targeting is sound. Hope this helps.

Hi’, I was wondering is a wrap-around mortgage the same or similar to this? Still trying to understand real estate. Looking for a house, not apartments. Thank You for your time DeDe

Hi DeDe – thanks for dropping a comment/question. A wrap around mortgage is not the same as assuming an existing mortgage that has already been created. For lack of a better term, a wrap around mortgage is a 2nd lien mortgage that is usually created by a home owner that is trying to seller-finance the equity of their home to a new buyer. The main reason that most seller-carry sellers do this is because they owe a an underlying balance to a bank or lender. They do this to avoid triggering their “Due on Sale” clause with their lender or bank. I hope this helps.

Hello, I had a quick question about this process. I am looking to buy a home, and I saw this being a great option at interest rates are extremely high. How would I go about contacting the seller? How do I know what this person pays on their mortgage and how much they owe on the house or what the starting loan balance was without asking?

Hi Charles – Thanks for the question. This question does not have an answer that is firm. The firmest answer I could give you is to search online for a seller in a area that you wish to explore that would be willing to have the mortgage assumed. Typically, the main reason someone would do this is because they are upside down on there equity which basically means they are stranded in the property because they will have to pay money out of pocket to sell. So instead of selling they would rather just let someone else step into their shoes and walk away from the headache, leaving that headache to you. Now, if your “pain tolerance” is higher, than this may not be a big deal for you. Especially if you are planning on living is said property for more than 5-10 years. Equity issues usually resolve themselves in that kind of time-horizon. That being said, if you engage in some type of arrangement like this, you would not be able to borrow against said property or possibly even sell it for some time. Keep in mind this is a hypothetical example, but an example that I have personally (anecdotally) seen many, many times in my 26 years of experience. Back to how this is done, I would scour chatrooms, real estate classified ads and even craigslist types of sites to see if someone is willing to walk away from their property for whatever reason. Then, you need to verify if their payments are on time by asking them to prove that they are by providing a Payoff Letter from their lender good for 30 days. This will show you if they have delinquent charges on their mortgage. If they are unwilling to do this, walk away – big red flag. Hope this is helpful and please, please, please, make sure you speak to an attorney or accountant before making this leap.