How to Sell a Promissory Note: Expert Tips

Jennifer Park

Published: March 20, 2018 | Updated: May 16, 2025

Selling a promissory note should not be a complicated undertaking. In fact, the overall process can be smooth and hassle-free when you prepare accordingly and use reputable note buyers or experienced note buying companies. As leaders in loan acquisitions and buying promissory notes, we have put together this functional guide to help you understand the ins and outs of “how to sell a promissory note.”

Key takeaways

- A promissory note is a written agreement between two parties and lists down all conditions of a transaction, often a loan.

- Careful record-keeping is essential when working with promissory notes.

- There are three main options for selling a promissory note: to an individual, to a family member, or to a note-buying company.

- A note-buying company will offer you a partial or full purchase of the remaining balance on loan.

- The entire process of selling a promissory note can take 15 to 35 days.

First, let’s lay the groundwork with some background information on notes in general.

What is a promissory note?

A promissory note is an agreement between a seller and a buyer, or a lender and a borrower, that lays out the terms and conditions of a transaction. It acts as a promise that the buyer (or borrower) will follow through with a set plan for repayment. However, a legal and proper promissory note is not a simple IOU. When prepared properly, they are official financial documents that are fully binding under the jurisdiction where they were entered.

Most traditional loan agreements like promissory notes (a.k.a. mortgage notes), especially in real estate or business loan transactions, are accompanied by a collateralizing document such as a mortgage, deed of trust or chattel mortgage (chattel used for personal property items), depending on the state in which the loan was originated.

In this case, the promissory note acts as the document that represents the loan repayment terms such as the payment amount, interest rate and amortization period, whereas the securing mortgage or deed of trust outlines the collateral securing the promissory note in question, such as the property and property laws under that specific state. Thus, the two documents make up the legal debt instrument.

Other types of promissory notes

Although promissory notes tend to be similar throughout the entire secondary mortgage market, there are minor differences in usages and applications. For instance, a consumer promissory note is an instrument that is either secured or unsecured. A consumer promissory note could be used for the purpose of a consumer lending transaction such as a borrower-occupied home or some type of personal property like a car, for example.

Other examples of promissory notes would be an escrow promissory note, which is a type of mortgage loan that contains an agreed-upon principal and interest payment which also includes monies for real estate taxes and insurance rolled into one. When taxes and insurance are collected alongside a mortgage payment, this is referred to as “escrowed” in the mortgage business.

Why is a promissory note used?

With the recent news of rising mortgage rates, seller-financed, owner-financed, or installment sales of property (both residential and commercial) should increase. Rising mortgage rates make sales difficult for both buyers and sellers alike. Buyers with less-than-perfect credit will seek ways around dealing with traditional lenders and their strict lending guidelines. Higher mortgage rates also mean that there are fewer highly-qualified buyers in the buying pool. Sellers can bypass the traditional lending route and use promissory notes to self-finance transactions.

Who uses promissory notes and how do they work?

Buyers: Promissory notes are advantageous to buyers who do not qualify for traditional mortgages because the seller acts as the bank and finances the loan. The trade off is a higher interest rate since the seller assumes a higher risk. The home (or business) serves as the collateral and an agreed upon down payment is the security for the note. As long as the buyer makes the agreed payments, they continue to have rights to the home. Should they default, the seller can take back, or foreclose on, the property.

Sellers: There are myriad reasons why a seller would choose to use a promissory note, also called carrying back a note. Sometimes when selling a property, it is the only choice available if the seller want to sell their real estate quickly. Family members often use promissory notes for ease of transferring and selling property, such as with tracts of farmland among siblings. Or note holders may have acquired promissory notes through divorce proceedings or inheritance. In some jurisdictions, a promissory note provides some advantages to the seller, such as being able to transfer the ownership of the note easily or being able to enforce the note more readily when and if a borrower defaults.

Why should I sell a promissory note?

Deciding to sell a note to a note buyer or a note buying company is one way to turn a non-liquid asset into a liquid asset in a short amount of time. Many sellers simply don’t want the risk of carrying a note long-term, and structure the sale with the intent of selling the real estate note as soon as possible. Even though they know note buyers and note-buying companies discount the price of notes to offset their risk based on the characteristics of the loan structure, sellers would rather have one lump sum of cash rather than take payments over time and wait 30 years, for example, for a return on investment.

Sometimes they don’t want the hassle of dealing with the IRS or the responsibility of managing the records and paperwork to keep track of the receivable asset they service. They could have an unforeseen emergency like medical bills or school tuition that may require them to liquidate the asset for cash in a timely fashion.

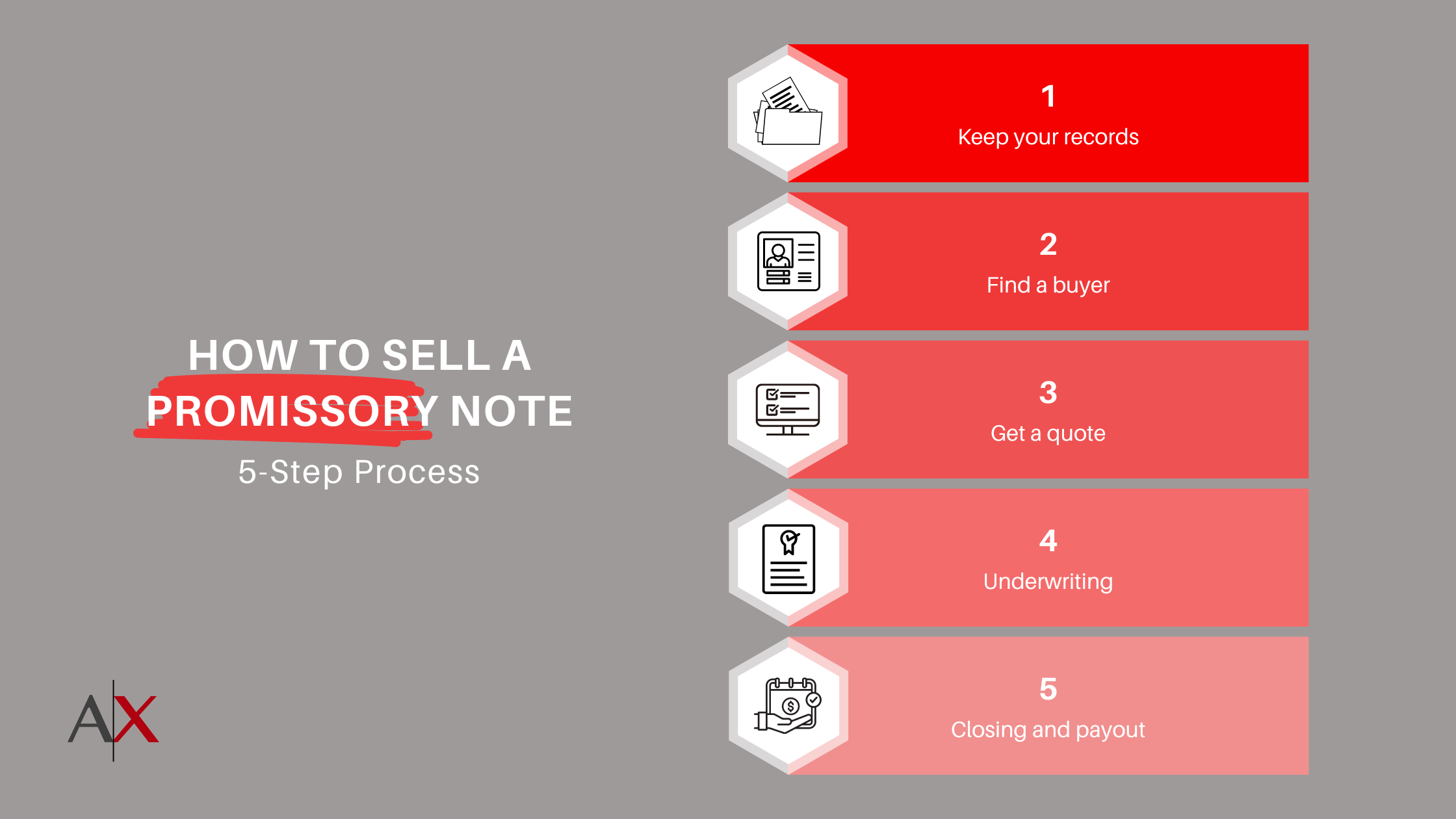

How do I sell my promissory note?

There are several factors involved in selling a note successfully. If selling a residential, commercial, or business note is in your near future, here are a few things to consider.

Record-keeping

If a seller should choose to use a promissory note, or if one is obtained through other means, other documents that may be present with a note are a mortgage, deed of trust or a real estate contract. All of the documents together represent the evidence of a transaction that can be used for legal and financial purposes such as sale or transfer. It’s important that all of the documents related to the sale be presented, so record-keeping is critical. This includes records of the down payment, number of payments made, taxes paid, insurance payments and policies, and all the specifics of the original note.

Where to sell a promissory note

Deciding who to sell your note to is one other decision that must be considered. Individuals will sometimes buy notes, although it is difficult to find individuals with enough cash on hand for such purchases. Individual note buyers often lack the experience to and know-how to make efficient deals, so proceed with caution.

Another option is to sell or transfer to someone you know, such as a family member. Finally, you can find reputable note-buying companies with established track records of buying notes. This is often the quickest and most seamless option. Do a search online or obtain a referral from your banker or realtor.

Getting a quote for a promissory note

To get a quote from a note buyer, you will need to answer a series of questions pertaining to the property. Prepare to provide information such as the property type, the property value, the buyer’s information, the buyer’s credit, the down payment amount, whether there are liens on the property, and how many payments have been made. After you supply this information, the note buying company will either offer you a partial purchase of a portion of the future payments, or a full purchase of the remaining balance. Remember that this amount will not be the full balance of the loan and is typically 65% to 90% of the value. The note buyer is assuming all of the risk of the loan. If you agree to the offer, the company will request the note paperwork and do an asset verification (collateral verification).

Underwriting and closing on a promissory note

Once the buyer receives all of the paperwork for underwriting, they will order an appraisal and do a title search performed during the course of the due diligence process. You should be sure that the company you work with is willing to pay for the costs associated with the purchase of your mortgage asset, including appraisal, broker price opinion (BPO) and title fees. With a clear title search, the closing can be scheduled either in person or via FedEx or UPS (if the note seller is out of state). The final step occurs when the seller receives their payment via wire transfer or check. The entire process can take anywhere from 15 to 35 days depending on your location, where the property is located, time to appraise, etc. Overall, it’s a relatively quick process from start to finish, in real estate terms.

As you can tell, the question of “how to sell a promissory note” is a loaded one. There’s a lot of expertise and knowledge used to properly handle every kind of promissory note, but we hope you’re left with a basic knowledge of how to sell a promissory note. If you have any questions or would like a quote, feel free to contact a note buyer today.

Frequently Asked Questions

Can I sell my mortgage note?

You can, but you will not receive the full value of the loan. Mortgage notes are typically sold at a discount, usually 65% to 90% of the value of the remaining payments.

Do I need a lawyer to sell my promissory note?

It’s not required, but recommended. A lawyer can help to ensure that the note is properly prepared and that all conditions of the sale are met.

How do I find someone to buy my promissory note?

You can search online or obtain a referral from your banker or realtor. You can also work with a reputable company, like Amerinote Xchange, that specializes in buying promissory notes.

Can I sell secured promissory note?

For a secured promissory note, where the repayment is backed by collateral such as real estate or another asset, you generally find a more straightforward path to selling. This is because the collateral adds a layer of security for the buyer, reducing their risk. Investors and companies that specialize in buying debt often see secured notes as attractive investments due to the assurance that they can recoup their money by seizing the collateral if the note isn’t paid.

Can I sell unsecured promissory note?

Selling an unsecured promissory note can be more challenging than selling a secured mortgage note. This is because unsecured notes are not backed by collateral, so they carry a higher risk for the buyer. You’ll need to demonstrate the creditworthiness of the borrower or offer the note at a discount to make it appealing. Buyers will likely conduct thorough due diligence, assessing the borrower’s financial history and the terms of the note.

What is the unsecured promissory note sales process?

The sales process of an unsecured promissory note generally involves several steps. Initially, you’d evaluate the note’s value, considering the interest rate, term, and borrower’s credit risk. Next, you might seek out potential buyers, which could include private investors, debt buying companies, or financial institutions.

Marketing your note effectively, perhaps through unsecured promissory note brokers who specialize in such financial instruments, can help find interested parties. Negotiations will follow, where terms such as price and transfer conditions are agreed upon. Finally, legal documents will need to be prepared and signed to transfer ownership of the note, ensuring that all legal requirements are met and that the new note holder has the right to collect the debt.

We Buy Promissory Notes

As a real estate debt, investment firm, we at Amerinote Xchange buy promissory notes, nationwide. Our dedicated capital is geared towards the purchase of first lien (1st, senior positions) and subordinated liens (2nd’s and other junior positions) across all fifty states and jurisdictions.

The promissory notes we buy are notes secured by any type of real estate whether performing (payments on time) or non performing (payments not on time). We would love to walk you through the price-discovery of you promissory note if you are thinking about bringing that asset to market.

Please feel free to reach out and contact us today for your no-obligation quote.

Hello my name is Michael,

I have been studying up on promissory notes/ bills of exchange/negotiable instruments for awhile and want to write one and then sell it. I found your website hoping this was the place to go. My comprehension of a note is that it is the same as cash. There are many cases that support that. Thing is, where do I start? My plan is to write only one or two and to retire on them. I appreciate any help you can offer.

Thank you

Hello Michael:

Thank you for your question. Here are some places to start

You can find good information on how to creating and holding a valuable mortgage notes here:

1. https://www.amerinotexchange.com/sell-mortgage-note/

2. https://www.amerinotexchange.com/how-a-partial-purchase-mortgage-note-offer-helps-with-taxes/

3. https://www.amerinotexchange.com/owner-finance-tips/

I hope this is helpful.

I have a promissory note that I want to transfer to my son. I am 75 yrs old and need my son to take care of all record keeping. The note is $390.00 per month, I would need my son to deposit $200.00 per month in my bank acct, the balance would be deposited in our joint bank acct. Does this sound like a good idea? What kind of forms would I need for this transaction?

Thank you for your help J

Hi Luella – thanks for your comment. I would not recommend conducting the payments distribution that way. There is a lot of room for error in the way you described.

I would recommend hiring a third-party, loan servicing company to distribute the funds according to your instructions. It may cost some extra money ($20 to $30 per month), but it is well worth it in the end. This way you do not have to worry record-keeping or tax-document preparation for interest collect. They will handle that for you in addition to distribution of payments.

Companies that we like are Madison Management Services (Reno), Allied Loan Servicing (Washington State), August REI (Texas) or any other loan servicing company that you prefer.

All in all, it is a cleaner method with way less headaches. If you have any other questions or remarks, please feel free to comment or contact us directly.

Thank you for your input, a third party is the way I will go

Hello

I am currently in the process of selling 5yrs of my note the thing is they will get a first on the whole note and property,i seen this a bit late,what happens to balance owed to me if the tenant has to be foreclosed on? the company i am dealing with said they would only want there owed part and i would get the rest,how would that work?

Thank you

Hi Bruce – thank you for your question. I am surprised the company you are working with cannot provide a sufficient answer for your on this question, but I will try to fill in the gaps for you. Typically and at least with us, when you transfer the whole loan to the new buyer on a partial purchase (in your case, 5 year payment stream), the are several ways to telegraph to the world that you are still in the deal even though the loan transferred to them. With our company, we have the note seller sign Purchase and Sale agreement / the assignment of mortgage or deed of trust and the promissory note endorsement (aka an allonge) at closing. In addition we have some called a Memorandum of Interest or Remainder Interest document signed basically stating that you have a remainder interest in the note, even though you are not the legal owner for the 5 year period that you sell the stream of payments. In addition to the documents I jsut mentioned you would also receive a amortization schedule showing the payment breakdown to you and us over that 5 year period. So if the borrower defualts in month 23 of 60, and assuming the borrower has not made any principal reduction payments, you will know exactly how much (to the penny) you would be entitled to in the case of a foreclosure or default. The trick is that if the property market changes for the worse (as it is currently as of this writing), then there may be additional risk because the equity cushion has or is getting smaller. So, in a foreclosure the note buyer will pay attorney fees, carrying costs, taxes, and potential additional fees that may be brought to bear by the borrower’s side if there is a mounted defense. After the property is recovered or the loan amount is recovered from the auction of the property due to a foreclosure action, the fees the buyer pays during the long and arduous process (in most states) are typically removed from total proceeds before you see a dim. What ever is left over will go to you. I hope this answers your question.